PROXY MONITOR

REPORT

Spring 2016

The Push for Proxy Access Continues

By James R. Copland

About the Author

JAMES R. COPLAND is a senior fellow at the Manhattan Institute, where he is director of legal policy[1]. In those roles, he develops and communicates novel, sound ideas on how to improve America's civil- and criminal-justice systems. Copland oversees MI's corporate-governance website, ProxyMonitor.org. In 2011 and 2012, he was named to the National Association of Corporate Directors “Directorship 100” list, which designates the individuals most influential over U.S. corporate governance.

Before joining MI, Copland was a management consultant with McKinsey and Company in New York. Earlier, he was a law clerk for Ralph K. Winter on the U.S. Court of Appeals for the Second Circuit. Copland has been a director of two privately held manufacturing companies since 1997 and has served on many public and nonprofit boards. He holds a J.D. and an M.B.A. from Yale University, where he was an Olin Fellow in Law and Economics; an M.Sc. in the politics of the world economy from the London School of Economics; and a B.A. in economics from the University of North Carolina at Chapel Hill, where he was a Morehead Scholar.

I. Introduction

Mid-April marks the start of corporate America's “proxy season,” when most large publicly traded companies hold annual meetings: 24 of the 250 largest U.S. companies[2] held annual meetings during January 1–April 15, another 37 will meet before the end of April, and most others will hold meetings by the end of June.

The annual meeting cycle gets its name from the proxy ballots distributed by publicly traded companies to their equity shareholders under rules promulgated by the Securities and Exchange Commission (SEC);[3] voting by proxy is the ordinary mechanism whereby common shareholders of corporations, who typically do not attend shareholder meetings, exercise their voting rights. Such proxy ballots may contain not only items proposed to the shareholders by the corporation—such as the election of directors, the appointment of independent auditors, and changes to the corporation's voting rules or corporate structure—but also shareholder resolutions, which can be introduced by any shareholder holding equity valued at $2,000 or more for at least one year.[4]

In 2016, as in 2015, the most significant proxy issue generated through the shareholder-proposal process will be “proxy access,” the idea that shareholders should have the right to place their own nominees for director on corporate proxy ballots to compete with boards' own director nominees. In November 2014, the office of New York City comptroller Scott Stringer—an elected official who oversees the pension fund assets that underlie retirement benefits for the city's public employees[5]—announced that proxy access would be the linchpin of a new “Boardroom Accountability Project” purportedly designed “to ensure that companies are truly managed for the long-term.”[6]

In 2015, the New York City funds introduced shareholder proposals seeking proxy access at 75 companies.[7] This effort largely succeeded in currying shareholder support: among the Fortune 250 companies, two-thirds of all shareholder proposals seeking proxy access received majority shareholder support in 2015, compared with 3.5 percent of all other shareholder proposals.[8] According to the comptroller's office, through the end of 2015, “109 companies have enacted viable proxy access bylaws since the launch of the project, either in response to a shareowner proposal or proactively, including 78 companies between October and December 2015.”[9]

This report gives a final review of the 2015 proxy season and previews the 2016 season, examining both the campaign for proxy access and shareholder proposals more broadly. Empirical evidence is based on data in the Manhattan Institute's Proxy Monitor database, available online at ProxyMonitor.org, which catalogs shareholder proposals submitted to the 250 largest U.S. publicly traded companies by revenues, as ranked by Fortune magazine (see box)[10]. Key findings about 2016's early proxy filings and returns include:

- The number of shareholder proposals is up. The average Fortune 250 company with an annual meeting scheduled by April 30, 2016, has faced 1.42 shareholder proposals, up 7.5 percent from all of 2015 and up 48 percent from the comparable period in 2015.

- Proxy-access proposals have been less likely to receive majority shareholder votes. Four of ten proxy-access proposals coming to a vote so far in 2016 have received majority support, down from 67 percent in all of 2015. In each of the six cases in which the proposal received less than majority support, the company adopted its own proxy-access bylaw, with different specifications from the shareholder proposal's specification.

- No other shareholder proposal has received majority support to date. In 2016, only four shareholder proposals involving issues other than proxy access have received more than 30 percent support. Three were at a single company, Emerson Electric. The other, which received 35 percent shareholder support at Walt Disney, sought to eliminate supermajority voting provisions from the company's bylaws.

Section II of this report summarizes 2015 shareholder-proposal activity, sponsorship, subject matter, and voting results. Section III previews the 2016 season, based on the 61 Fortune 250 companies with annual meetings scheduled by April 30 and the early voting results at the 21 of those companies that held annual meetings by March 31. Section IV highlights upcoming annual meetings at which shareholder-proposal items of interest—proxy-access proposals, proposals to separate corporate chairman and CEO positions, proposals relating to corporate political spending or lobbying, and environmental proposals—will come up for a vote.

About Proxy Monitor

The Manhattan Institute's Proxy Monitor database, launched in 2011, is the first publicly available database cataloging shareholder proposals and Dodd-Frank-mandated executive-advisory votes[11] at America's largest companies. The database is overseen by Margaret M. O'Keefe, who has more than two decades' experience in executive-compensation, corporate-governance, and proxy-advisory consulting. This is the sixth annual report previewing the annual proxy season and the 36th publication in a series of findings and reports by Manhattan Institute legal policy director James R. Copland, each drawing upon information in the database to examine shareholder activism in which investors attempt to influence corporate management through the shareholder-proposal process.

|

II. 2015 Shareholder Proposals

Number of Proposals

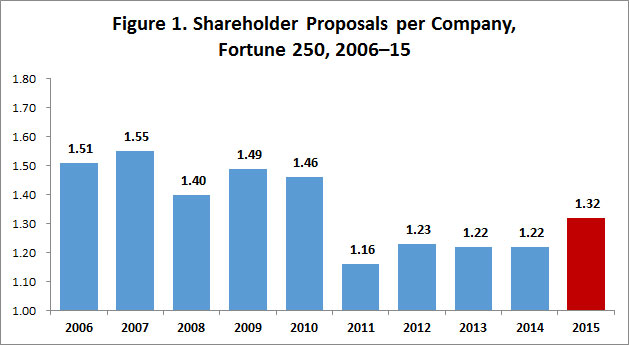

In 2015, the average Fortune 250 company faced more shareholder proposals, on average, than in any year since 2010 (Figure 1). (In 2010, Congress enacted the Dodd-Frank law, which mandated that companies hold annual, biennial, or triennial shareholder-advisory votes on executive compensation[13]. Proposals seeking such votes had been commonplace previously but were obviated by the Dodd-Frank rule.) Overall, the 250 largest American companies faced 330 shareholder proposals in 2015, up from 305 in 2014 and 306 in 2013. Eighty percent of the year-over-year increase in shareholder-proposal submissions can be accounted for by increased activity on the part of the New York City pension funds, chiefly through Comptroller Stringer’s Boardroom Accountability Project. Indeed, the increased number of proxy-access proposals filed in 2015 was 116 percent of the year-over-year increase in shareholder-proposal submissions—so the number of shareholder proposals sponsored, apart from proxy access, declined slightly.

Source: ProxyMonitor.org

Proposal Sponsors

As was the case in each of the nine prior years in the Proxy Monitor database, a small group of shareholders dominated the process of introducing shareholder proposals in 2015. Shareholder-proposal activists largely fall into three groups:

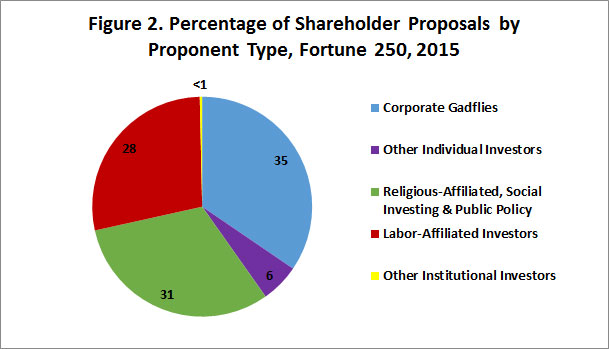

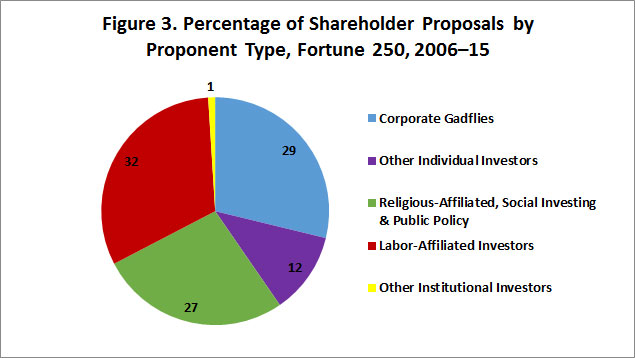

- Corporate Gadflies. A small number of individuals and their family members repeatedly file similar shareholder proposals at many companies. Such investors are commonly called “corporate gadflies.”[14] The five most active gadfly investors in 2015 sponsored 35 percent of all shareholder proposals (Figure 2), up from 29 percent annually over the full 2006–15 period (Figure 3). In 2015, three of these individuals and their family members—John Chevedden, William Steiner (and son Kenneth), and James McRitchie (and wife, Myra Young)—sponsored 32 percent of all shareholder proposals.

- Social Investors. A variety of institutional investors that focus on “socially responsible” investing[15], as well as various retirement and investment vehicles associated with religious or public-policy organizations, sponsored 31 percent of shareholder proposals in 2015, up from 27 percent annually across the broader ten-year period. Although orders of nuns and other religious institutions have become somewhat less active in sponsoring shareholder proposals in recent years, specific social-investing funds have become more active, as they have added shareholder proposals related to corporate political spending and lobbying to their long-standing focus on environmental and human-rights concerns.

- Labor-Affiliated Investors. Labor-affiliated pension funds that commonly sponsor shareholder proposals are one of two kinds: “multiemployer” plans affiliated with labor unions, such as the American Federation of Labor–Congress of Industrial Organizations (AFL-CIO); and state and municipal pension plans holding assets in trust for public employees, such as the New York City pension funds. (Corporate-sponsored private pension plans almost never file shareholder proposals.) In total, labor-affiliated pension plans sponsored 28 percent of shareholder proposals introduced at Fortune 250 companies in 2015—down from 32 percent annually over the broader 2006–15 period, notwithstanding the New York City funds’ proxy-access push. In recent years, private multiemployer pension plans affiliated with labor unions have been generally less active than they were previously in sponsoring shareholder proposals.

Source: ProxyMonitor.org

Source: ProxyMonitor.org

Aside from this small group of shareholder-proposal activists, very few stockholders introduce proposals. Individuals other than the five most active gadflies sponsored just 6 percent of all shareholder proposals in 2015, down from 12 percent annually in the broader 2006–15 period. Institutional investors without a connection to public- or private-employee pensions or a social, religious, or policy orientation sponsored less than 1 percent of shareholder proposals in 2015, in keeping with historical norms.

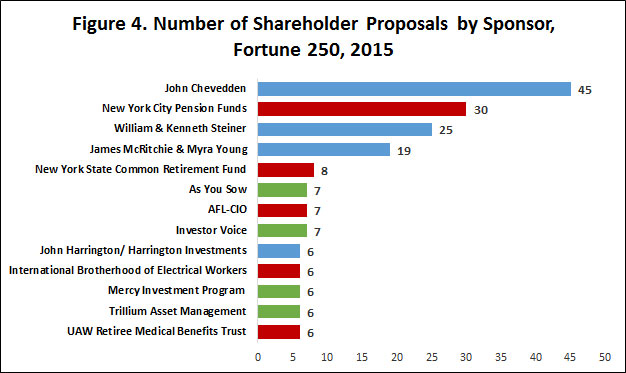

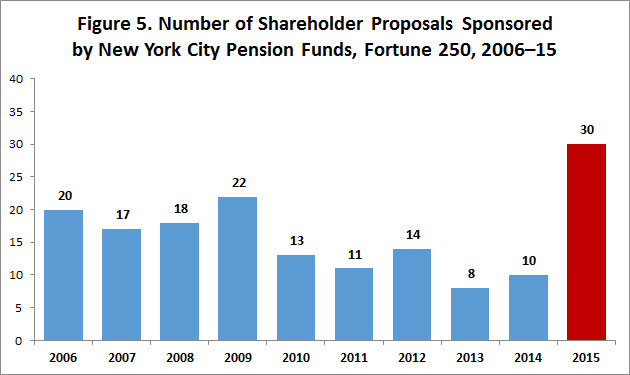

Overall, the most active sponsors of shareholder proposals were the three principal gadflies and the New York City pension funds. These investors each sponsored 19–45 shareholder proposals at Fortune 250 companies (Figure 4). No other single investor sponsored ten or more proposals, though nine different investors sponsored six to eight. Although the New York City pension funds have historically been active in sponsoring shareholder proposals, the push for proxy access in 2015 led to a substantial increase in such activity: at Fortune 250 companies, the New York City funds sponsored 30 shareholder proposals in 2015, up from ten in 2014 (Figure 5).

Source: ProxyMonitor.org

Source: ProxyMonitor.org

Proposal Subject Matter

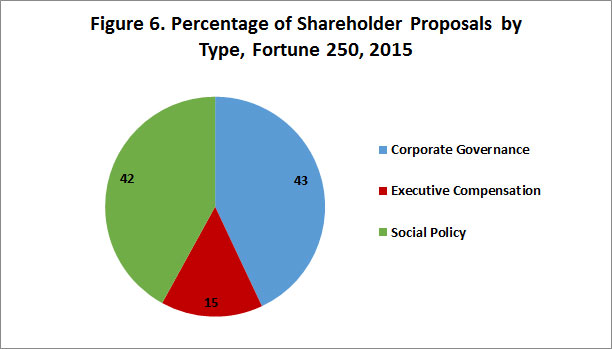

In 2015, the percentage of shareholder proposals devoted to corporate governance questions—including proxy access, rules for electing directors or taking other shareholder actions, and other questions of board structure and governance—were a plurality of all proposals, or 43 percent (Figure 6). Almost as many proposals, 42 percent of the total number introduced, involved social concerns with only an attenuated connection to shareholder value, such as corporate political spending or lobbying, environmental issues, and human rights. Proposals relating to executive compensation constituted 15 percent of all shareholder proposals in 2015.

Source: ProxyMonitor.org

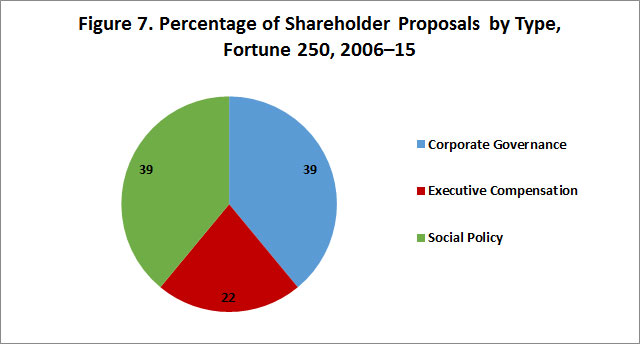

In general, the roughly 50–50 split between corporate-governance proposals and those related to social-policy issues is in keeping with historical norms: during the broader 2006–15 period, each class of proposal constituted 39 percent of all annual proposals (Figure 7). The percentage of shareholder proposals related to executive compensation is down as compared with the broader period, largely because proposals seeking shareholder-advisory votes on executive compensation, which were commonly introduced through 2010, were mooted by Dodd-Frank’s rule mandating such votes[16].

Source: ProxyMonitor.org

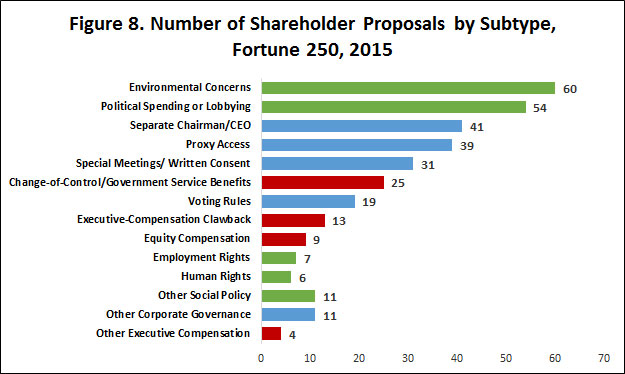

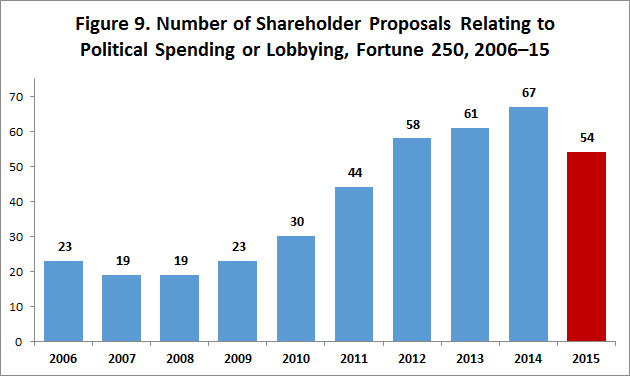

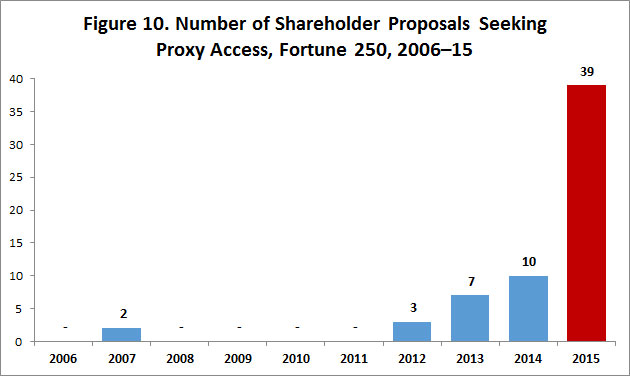

Although the broad classifications of shareholder proposals have changed little in the last decade, the specific types of proposal in each category have shifted. In 2015, the most common types of proposal involved environmental concerns, corporate political spending or lobbying, and separating the company’s chairman and chief executive roles (Figure 8)—types of proposals seen commonly throughout the broader 2006–15 period. The year 2015 saw the smallest number of political spending–related proposals since 2011, although such proposals were still the second-most commonly introduced type of proposal (Figure 9). Proposals seeking proxy access, which were very uncommon before 2014, were the fourth most common class of proposal in 2015 (Figure 10).

Source: ProxyMonitor.org

Source: ProxyMonitor.org

Source: ProxyMonitor.org

Voting Results

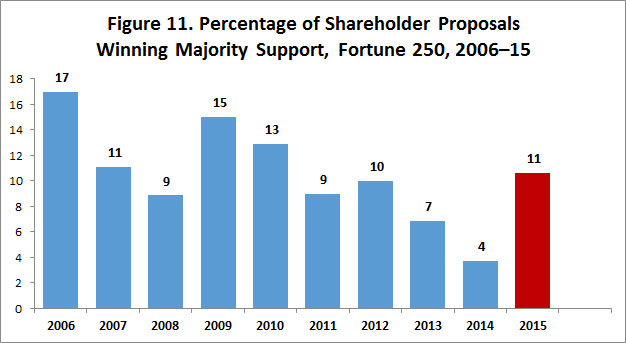

In 2015, 11 percent of shareholder proposals received majority shareholder support, up from 4 percent in 2014—and the highest level of support since 2010 (Figure 11). This increase, however, was wholly driven by the campaign for proxy access: two-thirds of the 39 proxy-access proposals introduced in 2015 received majority shareholder support, compared with just ten of 291 other proposals, or less than 4 percent (Figure 12).

Source: ProxyMonitor.org

Source: ProxyMonitor.org

Apart from the proxy-access proposals, eight of the ten proposals to receive majority shareholder support involved corporate governance: three seeking to permit the company’s shareholders to call special meetings (of ten introduced), two seeking to “declassify” board elections and elect all directors annually (of two introduced), two calling on the company to remove supermajority voting provisions from its bylaws (of five introduced), and one calling on the company to split its chairman and CEO roles (of 41 introduced). Two shareholder proposals seeking to eliminate accelerated vesting of equity compensation in the event of a change in corporate control—called “golden parachutes” by critics—also received majority support, among 25 such proposals introduced. No social or policy proposal received majority shareholder support; as noted in the year-end 2015 Proxy Monitor Report, no social policy–related proposal received majority shareholder support over board opposition at any Fortune 250 company during 2006–15.[17]

III. 2016 Early Filings and Voting Returns

In the first three months of 2016, 21 Fortune 250 public companies held annual meetings. These companies faced 34 shareholder proposals that came up for a vote. Another 40 companies are holding annual meetings in April, including 37 in the last two weeks of the month, as proxy season begins in earnest. From these early filings, and early voting returns, we can begin to form a picture of the 2016 proxy season—with the caveat that, historically, these companies have faced fewer shareholder proposals than the average company in the Proxy Monitor database.

Early Filing Data

The 61 Fortune 250 companies holding annual meetings by April 30, 2016, have faced 87 shareholder proposals—1.42 per company, on average, up from 1.32 per company in all of 2015. This 7.5 percent increase in the number of shareholder proposals introduced to date probably understates the overall rise in shareholder-proposal activity: in the comparable early periods of 2015 and 2014, the average company faced 0.96 and 0.98 shareholder proposals, respectively.

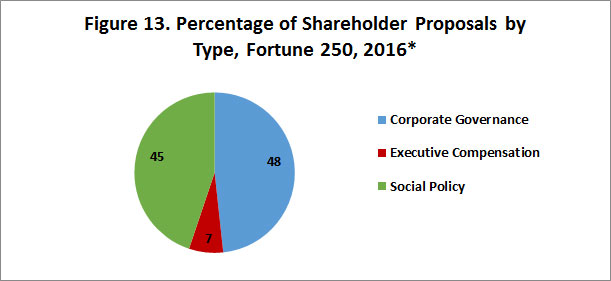

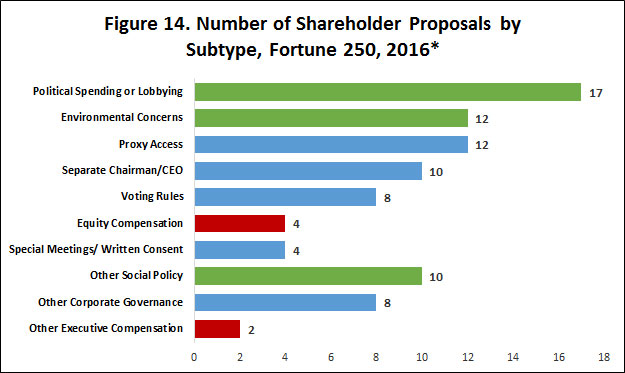

Among early-meeting companies, proposals remain somewhat evenly split between those relating to corporate governance (48 percent) and those relating to social-policy concerns (45 percent) (Figure 13). Only 7 percent of proposals to date have involved executive compensation. A plurality of proposals (17) have related to corporate political spending or lobbying, followed by those involving environmental concerns (12) and proxy access (12) (Figure 14).

*Among companies meeting by April 30, 2016

Source: ProxyMonitor.org

*Among companies meeting by April 30, 2016

Source: ProxyMonitor.org

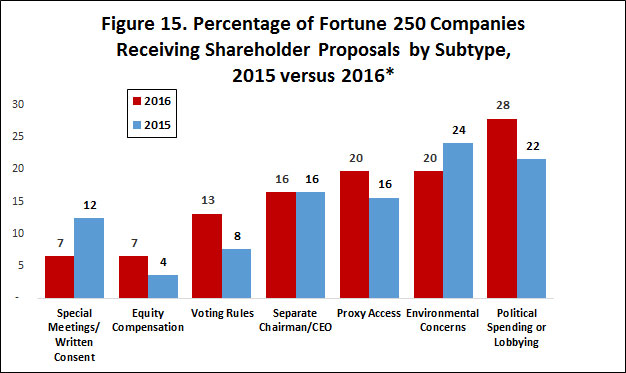

Compared with 2015 full-year totals, companies in 2016 have been more likely to receive shareholder proposals related to political spending or lobbying, proxy access, voting rules, and equity compensation (Figure 15). They have been less likely to receive shareholder proposals related to environmental concerns, or those seeking to empower shareholders to call special meetings or act through written consent. Notably, however, large oil and gas companies that typically see multiple environment-related proposals meet later in the proxy season.

*Among companies meeting by April 30, 2016

Source: ProxyMonitor.org

*Among companies meeting by April 30, 2016

Source: ProxyMonitor.org

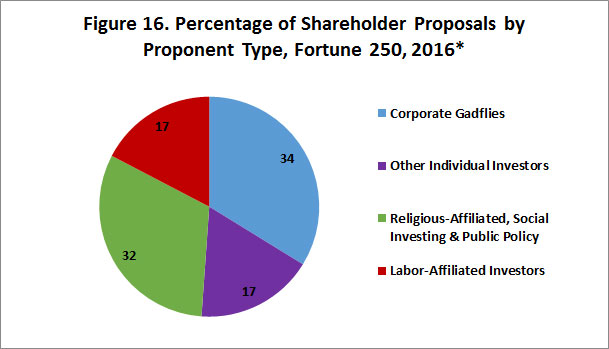

Among the early-filing companies in 2016, the traditional corporate gadflies have sponsored 34 percent of all shareholder proposals (Figure 16). And 17 percent of all proposals have been sponsored by other individual investors, though three of the 11 proposals were common proposals backed by a single individual, Jonathan Kalodimos, who is not a traditional gadfly; Kalodimos’s proposals encourage companies to adopt a policy of share repurchases in lieu of distributing cash dividends. A total of 32 percent of all shareholder proposals introduced to date were sponsored by social policy–oriented investors; and 17 percent by labor-affiliated pension funds.

Labor-affiliated investors have traditionally focused their efforts on the main proxy season. Indeed, the New York City pension funds have introduced only three shareholder proposals among the companies holding meetings by April 30. The increased incidence of shareholder proposals involving proxy access in 2016 is thus due to other shareholders introducing those proposals: the gadflies—Chevedden, Steiner, McRitchie, and Harrington—have each sponsored proxy-access proposals at companies meeting in the first four months of the year.

Early Voting Results

Through March 31, 21 Fortune 250 companies have held annual meetings, holding votes on 34 shareholder proposals at those companies. Four of those shareholder proposals received the support of a majority of shareholders, each seeking proxy access. In total, ten proxy-access proposals were on proxy ballots and came to a vote. Thus, 40 percent of all such proposals received majority shareholder support—down from 67 percent in all of 2015. In each of the six cases in which less than a majority of shareholders supported the shareholder proposal seeking proxy access, the company’s board of directors had adopted its own, differently structured, proxy-access rule.

Each of the six proposals sought proxy access for shareholders of 3 percent of outstanding shares, held for a minimum of three years, with the ability to nominate 25 percent of the board. All six companies instead adopted a proxy-access bylaw permitting election of no more than 20 percent of the board; Oshkosh also substituted a higher ownership threshold, equal to 5 percent of outstanding equity. None of the six companies with an unsuccessful shareholder proposal was on the list of companies targeted by the New York City comptroller’s office,[18] and four of the proposals were introduced by corporate gadflies Steiner and McRitchie, who lack large pension plans’ resources to solicit support. It will be interesting to see if this trend continues, among companies that adopt their own proxy-access proposals, as the proxy season unfolds with companies facing New York City–backed proposals.

Each of the ten proxy-access proposals coming to a vote so far in 2016 has received at least 30 percent shareholder support. Only four other shareholder proposals have achieved this level of support. Three were at a single company, Emerson Electric—involving corporate lobbying, sustainability, and greenhouse-gas emissions. The other, at Walt Disney, sought to eliminate supermajority voting provisions from the company’s bylaws—a proposal type that has received significant shareholder support, including majority votes, at companies in the past. The Disney proposal received 35 percent shareholder support.

IV. Upcoming Meetings to Watch

During April 19–30, 37 Fortune 250 companies will hold annual meetings, including nine large companies—AT&T, Citigroup, Coca-Cola, Dupont, IBM, General Electric, Honeywell, Johnson & Johnson, and Pfizer—that each face at least three shareholder proposals. (Johnson & Johnson and Pfizer each face four, Citigroup five, and GE six.) Among the 51 shareholder proposals that these 37 companies will face in the last two weeks of April, only two seek proxy access. Among the other most introduced classes of shareholder proposals coming to votes during this period, seven seek to split the company’s chairman and CEO roles, 11 involve political spending or lobbying, and five involve environmental issues.

Proxy Access

Two companies meeting in late April face proxy-access proposals, each sponsored by the New York City pension funds:

- PACCAR—April 26

- NRG Energy—April 28

PACCAR also received a proxy-access proposal from the New York City pension funds in 2015, which failed to garner majority shareholder support—winning 42 percent of the vote. This is NRG’s first proxy-access proposal; its board of directors has taken no position for, or against, the proposal.[19]

Splitting Chairman and CEO Roles

Seven shareholder proposals seeking to separate companies’ chairman and CEO positions are going to be considered by shareholders at Fortune 250 companies’ meetings between April 19 and April 30, six of which were sponsored by corporate gadflies Gerald Armstrong, John Chevedden, and Kenneth Steiner:

- U.S. Bancorp—April 19

- Honeywell—April 25

- IBM—April 26

- General Electric—April 27

- Johnson & Johnson—April 28

- Wells Fargo—April 28

- AT&T—April 29

Honeywell, Johnson & Johnson, U.S. Bancorp, and Wells Fargo also received similar proposals in 2015; none received majority shareholder support.

Political Spending and Lobbying

Ten Fortune 250 companies will face 11 shareholder proposals in the last two weeks of April that involve corporate political spending or lobbying. These proposals were sponsored by a mix of public-employee pension funds (for New York City and State, Philadelphia, and the Change-to-Win investment group) and social-investing vehicles (the Christopher Reynolds Foundation, the National Center for Public Policy Research, Trillium Asset Management, and Walden Asset Management). These upcoming meetings are:

- Honeywell—April 25

- Citigroup—April 26

- IBM—April 26

- Coca-Cola—April 27

- General Electric—April 27

- Johnson & Johnson—April 28

- Wells Fargo—April 28

- NRG Energy—April 28

- Pfizer—April 28

- AT&T—April 29

AT&T faces two separate proposals, one involving corporate political spending and one involving corporate lobbying.

Environmental Issues

Four Fortune 250 companies will face five proposals in the last two weeks in April that involve environmental concerns. These proposals concern various topics: climate change, environmental accident-risk reduction, deforestation in the company’s supply chain, and the “safe disposition by users of prescription drugs to prevent water pollution.”[20] The upcoming meetings at which these proposals will come to a vote are:

- AES Corp.—April 21

- Dupont—April 27

- Johnson & Johnson—April 28

- Berkshire Hathaway—April 30

Dupont faces two proposals, one relating to accident-risk reduction and the other to supply-chain deforestation.

V. Conclusion

So far in 2016, large publicly traded companies are facing more shareholder proposals—driven by an increase in proposals involving proxy access, corporate political spending or lobbying, equity-compensation plans, and voting rules. Only those proposals involving proxy access have won majority shareholder support, though the percentage of proxy-access shareholder proposals winning such support is lower than in 2015. Notably, however, each company for which a majority of shareholders have failed to support a shareholder proxy-access proposal has adopted its own proxy-access rule, differing somewhat from that proposed by shareholder activists. Thus, companies may have the ability to tailor such rules even if shareholders broadly support some form of proxy access.

Upcoming votes on proxy-access proposals merit close attention as the proxy season unfolds. Whether such rules become invoked in practice remains to be seen. How they may affect share value warrants ongoing study, too.

Endnotes

- Copland owns a diversified investment portfolio that may include, in small-percentage concentrations, the equities of companies named in this or other Proxy Monitor reports.

- The Manhattan Institute’s Proxy Monitor database includes the 250 largest publicly traded companies by revenues, as listed by Fortune magazine. Although this report loosely refers to this list as the “Fortune 250,” the fact that several of the Fortune 250 companies are not publicly traded means that some of the companies among the 250 largest that are subject to the proxy rules of the SEC are from the broader Fortune 300 group.

- Although corporate governance in the U.S. is mostly governed by substantive state law, cf. Del. Code Ann., tit. 8, § 211(b) (2009) (noting that in addition to the election of directors, “any other proper business may be transacted at the annual meeting”), the federal SEC controls the process of proxy solicitation under rules promulgated under section 14(a) of the Securities and Exchange Act of 1934, 4, Pub. L. No. 73-291, ch. 404, 48 Stat. 881 (1934).

- See 17 C.F.R. § 240.14a-8 (2007) [hereinafter “14a-8”].

- See Office of the State Comptroller, Fiduciary Responsibilities of the Comptroller, http://www.osc.state.ny.us/pension/fiduciary.htm (last visited Apr. 8, 2016). Full fiduciary authority over the funds rests with various boards composed of political and union delegates. For example, the board of the $43 billion New York City Employees’ Retirement System (NYCERS) includes the comptroller, the public advocate, a mayoral representative, each of the five New York City borough presidents, and three union delegates. See NYCERS, Board of Trustees, http://www.nycers.org/(S(azvv04mpy1qd2j5515dyny55))/about/Board.aspx (last visited Apr. 8, 2016).

- New York City Comptroller, Boardroom Accountability Project, http://comptroller.nyc.gov/boardroom-accountability (last visited Mar. 30, 2016); see also Press Release, Comptroller Stringer, NYC Pension Funds Launch National Campaign to Give Shareowners a True Voice in How Corporate Boards Are Elected: New York City Pension Funds File 75 Proxy Access Shareowner Proposals to Kick Off the Boardroom Accountability Project, Nov. 6, 2014, https://comptroller.nyc.gov/newsroom/comptroller-stringer-nyc-pension-funds-launch-national-campaign-to-give-shareowners-a-true-voice-in-how-corporate-boards-are-elected (last visited Mar. 30, 2016).

- See id.

- In determining shareholder support for shareholder proposals, the Manhattan Institute counts votes consistent with the practice dictated in a company’s bylaws, consistent with state law. Some companies measure shareholder support by dividing the number of votes for a proposal by the total number of shares present and voting, ignoring abstentions. Other companies measure shareholder support by dividing the number of favorable votes by the number of shares present and entitled to vote—thus including abstentions in the denominator of the tally. Neither practice necessarily skews shareholder votes in management’s favor: whereas the latter method makes it relatively more difficult for shareholder resolutions to obtain majority support, it also makes it more difficult for management to win shareholder backing for its own proposals, such as equity-compensation plans.

Shareholder-proposal activists prefer to exclude abstentions consistently in tabulating vote totals, without regard to corporate bylaws; see Heidi Welsh, Accuracy in Proxy Monitoring, HLS Forum on Corporate Governance and Financial Regulation (Sept. 16, 2013), https://blogs.law.harvard.edu/corpgov/2013/09/16/accuracy-in-proxymonitoring-2 (critiquing the Proxy Monitor data set), which necessarily inflates apparent support for their proposals. But such a methodology is inconsistent with federal law. The SEC’s Schedule 14A specifies that for “each matter which is to be submitted to a vote of security holders,” corporate proxy statements must “[d]isclose the method by which votes will be counted, including the treatment and effect of abstentions and broker non-votes under applicable state law as well as registrant charter and bylaw provisions”—clearly indicating that corporations can adopt varying counting methodologies in assessing shareholder votes and that state substantive law governs the parameters of vote calculation. See Item 21, Voting Procedures, 17 C.F.R. § 240.14a-101, available at http://www.sec.gov/about/sched14a.pdf (last visited Sept. 11, 2015).

Under the state law of Delaware, where most large public corporations are chartered, “the certificate of incorporation or bylaws of any corporation authorized to issue stock may specify the number of shares and/or the amount of other securities having voting power the holders of which shall be present or represented by proxy at any meeting in order to constitute a quorum for, and the votes that shall be necessary for, the transaction of any business.” Del. Gen. Corp. L. § 216, available at http://delcode.delaware.gov/title8/c001/sc07 (last visited Sept. 11, 2015). As a default rule, absent a bylaw specification, Delaware law specifies that “in all matters other than the election of directors,” companies should count “the affirmative vote of the majority of shares of such class or series or classes or series present in person or represented by proxy at the meeting,” id. at 216(4)—the precise inverse of shareholder-proposal activists’ preferred counting rule.

The SEC staff has adopted a rule that for the very limited purpose of determining whether a proposal has met the “resubmission threshold” to qualify for inclusion on the next year’s corporate ballot—a permissive standard requiring merely a minimum 3 percent, 6 percent, or 10 percent vote, respectively, in successive years; see Amendments to Rules on Shareholder Proposals, Exchange Act Release No. 40,018; 63 Fed. Reg. 29,106, 29,108 (May 28, 1998) (codified at 17 C.F.R. pt. 240)—“[o]nly votes for and against a proposal are included in the calculation of the shareholder vote of that proposal,” ignoring abstentions. SEC Staff Legal Bulletin No. 14, F.4., July 13, 2001, https://www.sec.gov/interps/legal/cfslb14.htm (last visited Apr. 8, 2016). Because this is a staff rule not voted on by the commission, because it exists for a limited purpose (with multiple rationales, including reducing workload in processing 14a-8 no-action petitions and adopting a permissive standard for ballot inclusion), and because it contravenes clear and long-standing deference to substantive state law in the field of corporate governance, the notion that this limited SEC staff vote-counting rule should dictate counting methodology, irrespective of state law and governing corporate bylaws, is untenable. Indeed, in 2014 and 2015, various shareholder proponents have introduced proposals seeking to modify companies’ bylaws to treat abstentions as non-votes; such proposals have received less than 10 percent shareholder support.

- Press release, Comptroller Stringer, New York City Funds, Announce Expansion of Boardroom Accountability Project, Jan. 11, 2016, http://comptroller.nyc.gov/newsroom/comptroller-stringer-new-york-city-funds-announce-expansion-of-boardroom-accountability-project (last visited Mar. 30, 2016).

- Cf. Fortune 500, http://fortune.com/fortune500 (last visited Mar. 30, 2016).

- Under the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010, publicly traded companies must hold shareholder-advisory votes on executive compensation annually, biennially, or triennially, at shareholders’ discretion. See Pub. L. No. 111-203, 124 Stat. 1376, §951 (2010) [hereinafter “Dodd-Frank Act”].

- See Reports and Findings, http://www.proxymonitor.org/Forms/reports_findings.aspx (last visited Mar 30, 2016).

- See Dodd-Frank Act, supra note 11.

- “Corporate gadflies,” as commonly used in Charles M. Yablon, Overcompensating: The Corporate Lawyer and Executive Pay, 92 COLUM. L. REV. 1867, 1895 (1992); and Jessica Holzer, Firms Try New Tack Against Gadflies, WALL ST. J. (June 6, 2011), http://online.wsj.com/article/SB10001424052702304906004576367133865305262.html.

- See Michael Chamberlain, Socially Responsible Investing: What You Need to Know, FORBES (Apr. 24, 2013), http://www.forbes.com/sites/feeonlyplanner/2013/04/24/socially-responsible-investing-what-you-need-to-know (“In general, socially responsible investors are looking to promote concepts and ideals that they feel strongly about”).

- See Dodd-Frank Act, supra note 11.

- See James R. Copland & Margaret M. O’Keefe, Proxy Monitor 2015: A Report on Corporate Governance and Shareholder Activism (Manhattan Inst. for Pol’y Res., Fall 2015), http://www.proxymonitor.org/pdf/pmr_11.pdf. See also James R. Copland, Getting the Politics Out of Proxy Season, Wall St. J., Apr. 23, 2015, http://www.wsj.com/articles/getting-the-politics-out-of-proxy-season-1429744795. Note that this statement holds true for the current Fortune 250, but a shareholder proposal at KBR, Inc. did receive 55 percent shareholder support over board opposition in 2011, when the company was on the Fortune 250 list. That proposal, sponsored by the New York City pension funds, encouraged the board to amend the company’s equal-employment-opportunity policy to prohibit discrimination based on sexual orientation.

- See Boardroom Accountability Project 2016 Company Focus List, http://comptroller.nyc.gov/boardroom-accountability/2016-focus-boardroom-accountability (last visited Apr. 4, 2016).

- NRG Energy, Inc., Proxy Statement Pursuant to Section 14(a) of the Securities Exchange Act of 1934, proposal no. 5 (Mar. 16, 2016), https://www.sec.gov/Archives/edgar/data/1013871/000104746916011231/a2227688zdef14a.htm#do75203_proposal_no._5_stockho__do702355.

- Johnson & Johnson, Proxy Statement Pursuant to Section 14(a) of the Securities Exchange Act of 1934, proposal no. 7 (Mar. 16, 2016), https://www.sec.gov/Archives/edgar/data/200406/000119312516505952/d110075ddef14a.htm#toc110075_44.