PROXY MONITOR

REPORT

2014 Proxy Season Midterm Report

Management winning more votes in 2014, as greater

percentage of shareholder proposals focus on social and political issues

By James R. Copland

ABOUT PROXY MONITOR

The Manhattan Institute launched its Proxy Monitor project in 2011 to study shareholder resolutions on corporate proxy ballots, as well as shareholder advisory votes on executive compensation—then newly required for all publicly traded companies under the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010.[1] At the heart of the project is the ProxyMonitor.org online database, which contains information on all shareholder proposals on the proxy ballots of the 250 largest American companies by revenues, dating back to 2006, in addition to executive-compensation advisory vote totals. ProxyMonitor.org is the first publicly available, searchable resource of its kind.

|

During corporate America’s “proxy season,” between April 15 and the end of June, most of America’s largest publicly traded corporations hold their annual meetings to vote on company business—as well as on various proposals introduced by shareholders, which appear on proxy ballots under regulations promulgated by the Securities and Exchange Commission. By the end of May, a clear picture of the proxy season has emerged: among the 250 largest U.S. public companies by revenues that constitute the Manhattan Institute’s ProxyMonitor.org database, 212 had scheduled meetings by May 30, and 188 had held meetings by May 23.[3]

In 2014, companies have faced a similar number of shareholder proposals, on average, as in 2013, 2012, or 2011; at the same time, shareholders have supported a smaller percentage of these proposals than in any previous year in the Proxy Monitor database (which dates back to 2006). In part, the drop in support for shareholder proposals is attributable to more proposals being devoted to social or political issues than to matters of corporate governance or executive compensation, as investors with a “social investing” orientation sponsored a greater percentage of shareholder proposals in 2014. The most commonly introduced type of proposal, as in 2013 and 2012, involved companies’ political spending or lobbying, but none of these proposals passed—the case, absent management support, in each of the eight years covered by ProxyMonitor.org—while shareholder support for such proposals has averaged only 19 percent, essentially unchanged from 2012.

This latest Proxy Monitor finding discusses these results in more detail. First, it looks at the rate of introduction of shareholder proposals, including shareholder proposal sponsorship and the types of proposals being introduced. Next, it examines voting results, also including vote results for management-sponsored proposals seeking shareholder advisory votes on executive compensation (now required annually, biennially, or triennially, under Dodd-Frank). Finally, it looks, in greater depth, at voting results for proposals involving political spending or lobbying.

I. 2014 Shareholder Proposal Trends

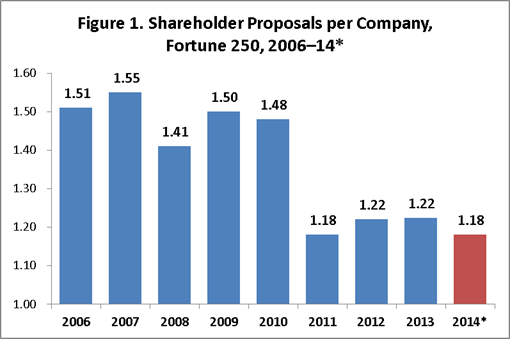

In 2014, the number of shareholder proposals introduced has fallen modestly (3 percent) from 2013: companies in the Fortune 250 have faced 1.18 proposals, on average, down from 1.22 (Figure 1). The number of shareholder proposals introduced is identical to that seen in 2011 and consistent with the rate of introduction over the last four years. (The number of shareholder proposals per company was markedly higher from 2006 through 2010—in part because companies faced many proposals seeking shareholder advisory votes on executive compensation; because such votes are now required under Dodd-Frank, there is no need for shareholder proposals seeking such votes.)

Source: Proxy Monitor

*As of May 30, 2014, 212 of 250 companies have filed proxy statements.

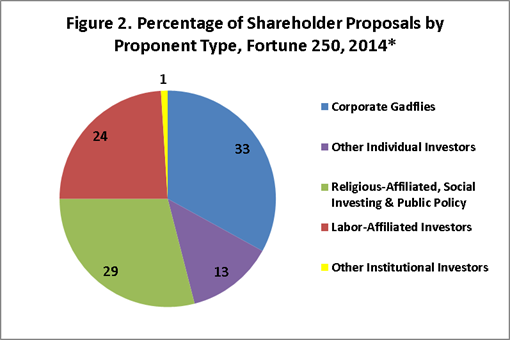

Shareholder Proposals by Proponent Type

Compared with 2013 and earlier years, more shareholder proposals in 2014 (Figures 2 and 3) have been introduced by investors with a religious, social, or public policy orientation, as well as by “corporate gadfly” individual investors (small investors who repeatedly file common classes of proposals across multiple companies). Indeed, one-third of all shareholder proposals introduced to date have been sponsored by just five gadfly investors and their family members: John Chevedden, Kenneth Steiner, James McRitchie, Gerald Armstrong, and Evelyn Davis. (The octogenarian Ms. Davis, previously among the most active sponsors of shareholder proposals, introduced none at Fortune 250 companies in 2013 and just one to date in 2014.) The number of shareholder proposals introduced by labor-affiliated pension funds in 2014, in contrast, is down significantly from 2013: only 24 percent of all shareholder proposals to date were sponsored by pension funds and other investment vehicles associated with public employees or multiemployer, private pension plans. In keeping with previous years, institutional investors without a labor affiliation—or a religious, social, or policy purpose—have sponsored 1 percent or less of all shareholder proposals. The only such proposal, to date, in 2014 was a poison-pill-redemption proposal at Navistar, introduced by GAMCO Investments, billionaire activist investor Mario Gabelli’s fund, which received the backing of 92 percent of shareholders after management failed to oppose it.

Source: Proxy Monitor

*As of May 30, 2014, 212 of 250 companies have filed proxy statements.

Source: Proxy Monitor

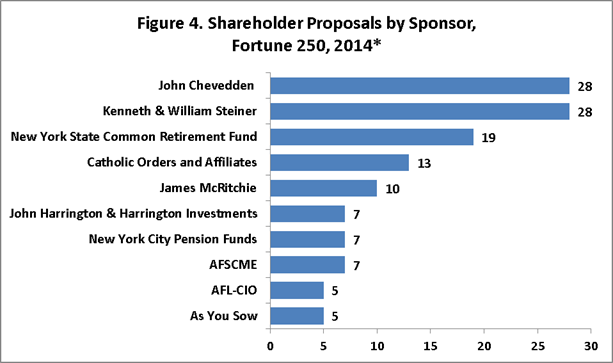

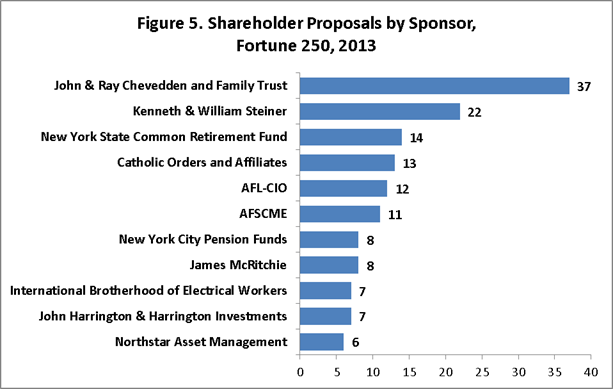

Shareholder Proposals by Sponsor

As in 2013, the most frequent individual sponsors of shareholder proposals have been John Chevedden and the father-son tandem of William and Kenneth Steiner. These gadfly investors’ proposals are generally very similar. Whereas Chevedden was the named sponsor of significantly more proposals in 2013, the Steiners and Chevedden have been the named sponsors of the same number of proposals this year (Figures 4 and 5). (As noted in Proxy Monitor’s 2014 winter report, various companies have been fighting back against Mr. Chevedden through litigation.)

The drop in activity from labor-affiliated pension funds in 2014 does not include public-employee funds for New York City and State. The most frequent sponsor of shareholder proposals in 2014—apart from Chevedden and the Steiners—is again the New York State Common Retirement Fund, which covers retirement obligations for non-teacher public employees of the state and most of its municipalities (except New York City). The sole fiduciary of this fund is New York State comptroller Thomas DiNapoli, an elected Democratic official. All but one of the New York State fund’s 19 shareholder proposals involved social or policy concerns, and 14 of the 19 involved corporate political spending or lobbying. The New York City pension funds, in contrast to the state fund, are governed by a board, with the elected comptroller, now Democrat Scott Stringer, serving as managing trustee. Stringer, likewise, appears to have adopted an activist stance (in keeping with predecessor John Liu), with the City’s funds sponsoring seven proposals to date in 2014, compared with eight in all of 2013.

Source: Proxy Monitor

*As of May 30, 2014, 212 of 250 companies have filed proxy statements.

Source: Proxy Monitor

The drop-off in labor-fund activity in sponsoring shareholder proposals in 2014 is principally explained by a decline in activity from multiemployer plans from private pension funds. The AFL-CIO’s pension fund, long one of the most significant sponsors of shareholder proposals, has sponsored only five to date in 2014, down from 12 last year; and the number of proposals sponsored by the International Brotherhood of Electrical Workers fund has dropped from seven to three. The United Brotherhood of Carpenters fund, long active in sponsoring shareholder proposals, has continued the reduction in such activity first observed in 2013, while leading sponsorship for only two proposals in 2014. The pension fund for the American Federation of State, County, and Municipal Employees (AFSCME)—which represents public employees across multiple jurisdictions—has also been somewhat less active this year, sponsoring only seven proposals to date, compared with 11 in 2013.

Shareholder Proposals by Type

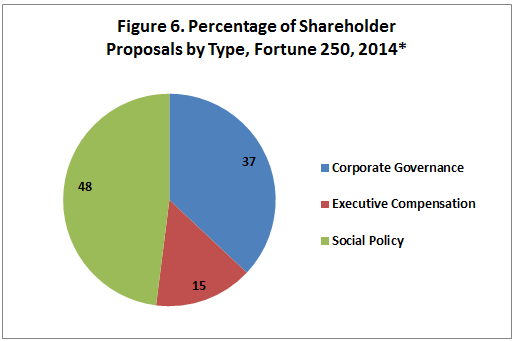

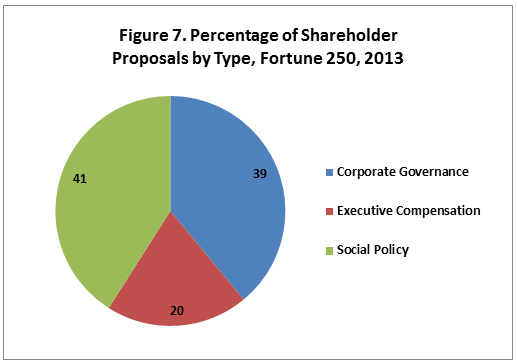

Perhaps unsurprisingly—given the increased level of shareholder proposal sponsorship among social investors and the politically oriented New York funds’ proportion of labor-affiliated shareholder proposal sponsorship—social and policy issues have constituted a higher percentage of shareholder proposals in 2014 than in previous years. Some 48 percent of all shareholder proposals introduced to date this year have involved social or policy concerns, up from 41 percent in 2013 (Figures 6 and 7).

Source: Proxy Monitor

*As of May 30, 2014, 212 of 250 companies have filed proxy statements.

Source: Proxy Monitor

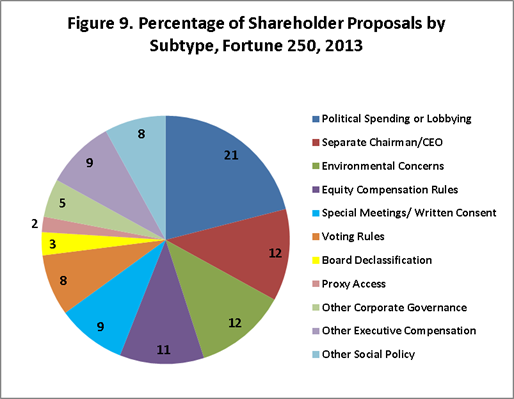

Shareholder Proposals by Subtype

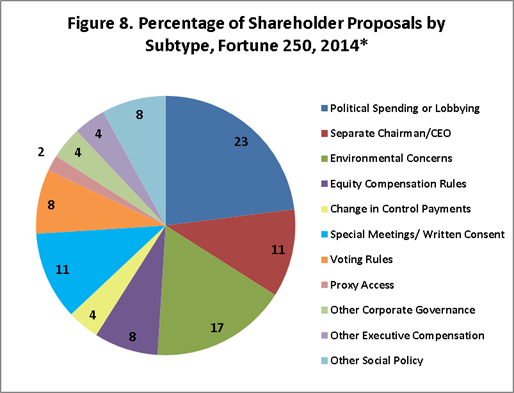

As in 2012 and 2013, shareholder proposals related to corporations’ political spending or lobbying constitute a plurality of all proposals introduced in 2014—up marginally to 23 percent, from 21 percent last year (Figures 8 and 9). The percentage of proposals related to environmental concerns is also up significantly, from 12 percent in 2013 to 17 percent this year. Other issues common on shareholder ballots in 2014, as in 2013, are proposals to separate the company’s chairman and chief executive officer positions, proposals related to managers’ equity compensation, and proposals to enable shareholders to act outside annual meetings, by calling special meetings or securing written consent.

Source: Proxy Monitor

*As of May 30, 2014, 212 of 250 companies have filed proxy statements.

Source: Proxy Monitor

II. Summary of Results

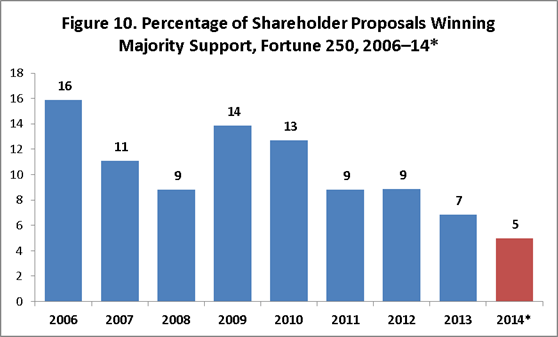

Only 5 percent of shareholder proposals have received the support of a majority of shareholders in 2014, down from 7 percent in 2013 (Figure 10). This low level of support is significantly below the support levels witnessed in any previous year in the Proxy Monitor database. Two factors principally explain this drop.

First, fewer Fortune 250 firms now face proposals most likely, in years past, to garner majority support, notably: eliminating “staggered” boards (i.e., where not all directors are elected annually); eliminating supermajority voting rules; and requiring the election of directors by a majority (as opposed to a plurality).[4] The drop in the number of such proposals is due largely to the broader adoption of these ideas at many of the largest companies;[5] as a consequence, fewer companies now face such proposals than in previous years.

In addition, companies that do face proposals likely to garner majority voting support seem to have become more likely, than in the past, to negotiate with the shareholder activists proposing them—and, in turn, voluntarily adopt such rules on their own (with the proposals thus withdrawn before proxy statements are released).[6]

Source: Proxy Monitor

*As of May 30, 2014, 212 of 250 companies have filed proxy statements.

Among the nine shareholder proposals to receive majority shareholder support among Fortune 250 companies voting by May 23, seven involved corporate governance questions; one involved executive compensation; and one involved social or policy concerns. The social-policy proposal, at Kraft Foods, was a “laudatory resolution” in support of animal-welfare standards sponsored by the Humane Society, calling on Kraft to work toward higher animal-welfare standards in its pork supply chain; the resolution was supported by management and received the support of 76 percent of voting shareholders. The executive-compensation-related proposal to win majority support was a proposal at Valero Energy seeking to modify the company’s equity-compensation vesting in the event of a change of control—called a “golden parachute” by plan critics—introduced by the labor-affiliated Amalgamated Bank; the proposal received the support of 55 percent of shareholders. The corporate-governance proposals to pass included three proposals seeking to end supermajority-voting requirements in company bylaws; three proposals seeking to permit shareholders to call special meetings; and GAMCO Investment’s anti-poison-pill provision, introduced at Navistar, which management supported. (On one of the majority-voting proposals to pass, introduced at Bristol-Myers Squibb by Kenneth Steiner, the board made no recommendation for or against the proposal, which consequently won the backing of 80 percent of shareholders.)

Political Spending and Lobbying Proposals

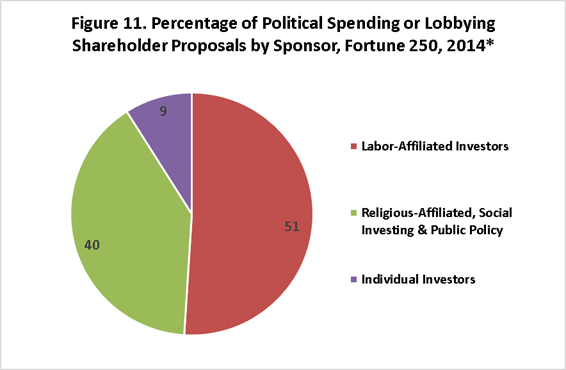

In contrast to shareholder proposals overall, the most commonly introduced shareholder proposals—those related to a company’s political spending or lobbying—have been overwhelmingly sponsored by labor-affiliated investors, as well as social and religious investors (Figure 11). A majority of these proposals have been backed by labor-affiliated pension funds, including 14 of the 19 proposals introduced by the New York State Common Retirement Fund and all seven of the proposals introduced by AFSCME. Three social-investing funds—Domini Social Investments, Trillium Asset Management, and Walden Asset Management—have also sponsored multiple shareholder proposals on this topic in 2014. Meanwhile, only five such proposals on the topic have been introduced by individual investors to date, with none sponsored by gadfly investors.[7]

Source: Proxy Monitor

*As of May 30, 2014, 212 of 250 companies have filed proxy statements.

As noted in a recent Wall Street Journal editorial on the subject,[8] most shareholders have continued to reject such proposals related to political spending or lobbying. Proposals in this class have received, on average, the support of 19.4 percent of shareholders in votes held through May 23—in keeping with (and marginally lower than) the percentage supporting such proposals in 2013. Notwithstanding this substantial shareholder opposition, however, certain companies have voluntarily changed disclosure practices under the pressure of various activists, including New York State comptroller DiNapoli and Bruce Freed, a former Democratic congressional staffer who now heads the Center for Political Accountability,[9] an organization devoted exclusively to this topic.[10]

Executive-Compensation Advisory Votes

In executive-compensation advisory votes, as in facing shareholder proposals, companies in the Proxy Monitor database have fared well in 2014. Among the 181 companies holding such votes by May 23, only one—TRW Automotive Holdings—received less than majority shareholder support (only 43.7 percent of TRW’s shareholders supported its executive compensation). In contrast, five companies received less than majority support for executive compensation in 2013. (To date, seven other companies have received majority support, but below the 70 percent threshold deemed significant by the proxy advisory firm Institutional Shareholder Services [ISS]; there were 17 such companies in all of 2013.) These results suggest that America’s larger companies have either fallen into line with the compensation methodologies backed by ISS and other proxy firms—or that they have done a better job at communicating the value of their compensation models to investors.

ENDNOTES

-

Pub. L. No. 111-203, 124 Stat. 1376, §951 (2010) [herein after Dodd-Frank Act].

- See Proxy Monitor, Reports and Findings, http://proxymonitor.org/Forms/reports_findings.aspx (last visited June 5, 2014).

- Twelve companies, whose annual meeting results appear in the Proxy Monitor database, were not in the Fortune 250 list for 2013and therefore are excluded from this analysis: Aon, Ashland, Coca-Cola Enterprises, Devon Energy, Eaton, ITT, KBR, Motorola, Oshkosh, Public Service Enterprise Group, Sempra Energy, and the Williams Companies.

- In 2014, with 212 of 250 companies reporting, ten shareholder proposals have called for simple majority voting or majority voting for director elections, as compared to 14 in 2013, 17 in 2012, and 20 in 2011. No shareholder proposals seeking to “declassify” staggered director terms have come up for a vote among Fortune 250 companies this year, as compared to eight such proposals in 2013, 12 in 2012, and six in 2011.

- For example, according the Harvard Shareholder Rights Project, which has advocated the proposal to declassify staggered board terms, two-thirds of the S&P 500 companies that had classified boards as of 2012 have now changed their practice. See 121 Companies Agreeing to Move toward Annual Director Elections, http://srp.law.harvard.edu/companies-entering-into-agreements.shtml (last visited June 12, 2014).

- For example, among companies facing board-declassification proposals introduced through efforts of the Harvard Shareholder Rights Project, 56 percent agreed to declassify their boards in 2012, 68 percent in 2013, and 76 percent in 2014. See id.

- One frequent-proposal sponsor, social investor John Harrington, did introduce one such proposal individually, as well as another by his social investing fund.

- Wall Street Journal Editorial Board, Good News in the Proxy Wars: The left's political disclosure campaign is falling flat, Wall St. J (May 25, 2014), available at http://online.wsj.com/news/articles/SB10001424052702303980004579576281696502364.

- See Center for Political Accountability, CPA staff, http://www.politicalaccountability.net/index.php?ht=d/sp/i/240/pid/240; see also Center for Political Accountability, Strong 2014 Proxy Season Begins with Three New Companies Adopting Political Disclosure, CPA Newsletter (Feb. 2014), http://www.politicalaccountability.net/index.php?ht=a/GetDocumentAction/i/8340.

- See Center for Political Accountability, About the CPA, http://www.politicalaccountability.net/index.php?ht=d/sp/i/870/pid/870/pid/190; see also Political Disclosure and Oversight Resolution 2013, http://www.politicalaccountability.net/index.php?ht=d/sp/i/867/pid/867 (last visited June 9, 2014).