PROXY MONITOR 2017

FINDING 1

Climate-Change Proposals Break Through

By James R. Copland and Margaret M. O’Keefe

Mr. Copland is a senior fellow with and director of legal policy at the Manhattan Institute.

Ms. O’Keefe is the Manhattan Institute’s Proxy Monitor project manager.

ABOUT PROXY MONITOR

The Manhattan Institute’s Proxy Monitor database, launched in 2011, is the first publicly available database cataloging shareholder proposals and Dodd-Frank-mandated executive-compensation advisory votes[1] at America’s largest publicly traded companies. Findings and reports by James R. Copland, Manhattan Institute senior fellow and director of legal policy, and Margaret M. O’Keefe, Proxy Monitor project manager, draw upon information in the database to examine shareholder activism in which investors attempt to influence corporate management through the shareholder-proposal process.[2] The conclusions in these reports are the authors’ own and do not reflect an institutional view of the Manhattan Institute.

|

Under rules promulgated by the Securities and Exchange Commission (SEC),[3] shareholders of publicly traded corporations listed in the United States may place items on company proxy ballots to be voted on at corporate annual meetings. Under current rules, shareholders must have held at least $2,000 in company shares for at least one year to propose a ballot item.[4]

In recent years, shareholder activists focused on social and environmental concerns have regularly used the shareholder-proposal process to advance ideas motivated primarily by social, economic, or policy concerns—which, under SEC rules, companies have been required to include on their proxy ballots since 1976.[5] In 2017, to date, such social-oriented proposals have constituted 56% of all shareholder proposals introduced on the proxy ballots of companies included in the Proxy Monitor database—the highest share dating back to the database’s first year, 2006.

Beyond the sheer numbers of environmental and other social-oriented shareholder proposals introduced in 2017, a subset of these proposals has received unprecedented shareholder voting support this year. For the first time in the 12 years tracked in the Proxy Monitor database, some environment-related shareholder proposals received majority shareholder support. Three substantively identical environment-related shareholder proposals introduced at oil or electricity companies—ExxonMobil, Occidental Petroleum, and PPL—each received the support of a majority of shareholders.

The proposals winning the support of shareholder majorities each asked the respective companies to “publish an annual assessment of the long-term portfolio impacts of technological advances and global climate change policies, at reasonable cost and omitting proprietary information . . . consistent with” government policies “to limit global average temperature rise to well below 2 degrees Celsius.” The proposals were predicated upon the November 2016 implementation of the December 2015 “Paris Agreement,” entered into at the 21st Conference of the Parties to the UN Framework Convention on Climate Change. The New York State Common Retirement Fund, which holds pension assets in trust for the New York State & Local Retirement System, was a sponsor of all three proposals and the lead sponsor of proposals at ExxonMobil and PPL; the California Public Employees Retirement System (CalPERS), which similarly holds assets in trust for California public employees, was the lead sponsor of the proposal at Occidental.

ExxonMobil and Occidental each received substantially the same proposal in 2016, when the proposals garnered 38% and 41% shareholder support at each company, respectively. In 2017, however, many large institutional investors shifted their votes—led by BlackRock, the world’s largest institutional investor,[6] which in March 2017 announced renewed commitment toward addressing climate change in its shareholder engagement.[7] BlackRock and other institutional investors were, in turn, reacting to a pressure campaign against fund families themselves by shareholder activists[8]—which may be a future trend in such campaigns.

This finding begins by analyzing holistically 2017’s environment-related shareholder proposals, followed by a discussion of this year’s increased support for shareholder proposals seeking company analysis of portfolio sensitivity to the Paris Agreement’s climate goals.

Overview of 2017 Environment-Related Shareholder Proposals

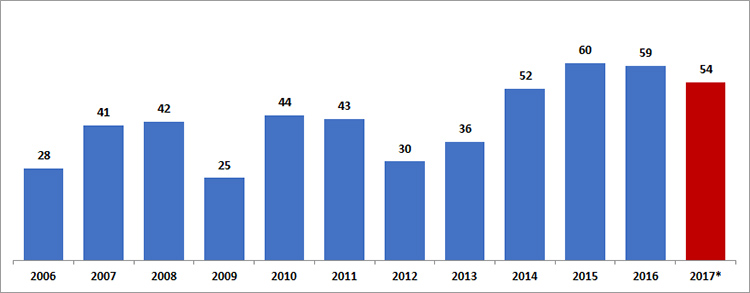

In each of the last four years, the 250 largest publicly traded companies, as tracked in the Proxy Monitor database, have faced more than 50 shareholder proposals relating principally to environmental concerns (Figure 1). Fifty-four such proposals have been placed on company proxy ballots to date among the 225 such companies filing proxy statements related to annual meetings held in the first half of the year; with 10% of companies outstanding, final year-end figures should be in line with 2016, when 59 such proposals were introduced, and 2015 (60).

Figure 1. Environment-Related Shareholder Proposals

Source: ProxyMonitor.org database

*In 2017, for 225 of 250 companies with annual meetings scheduled through the end of June

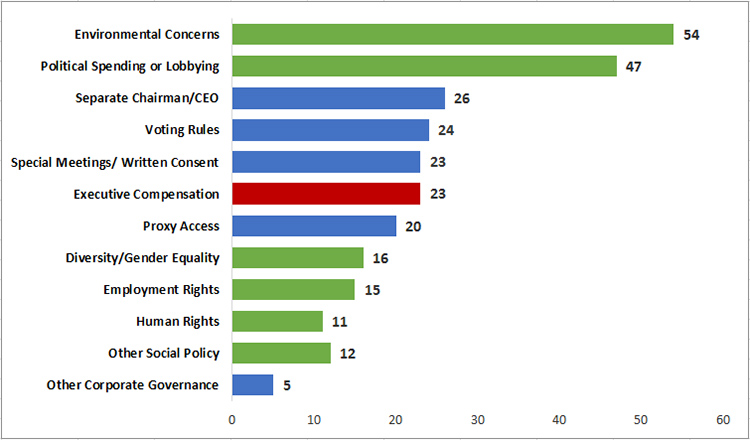

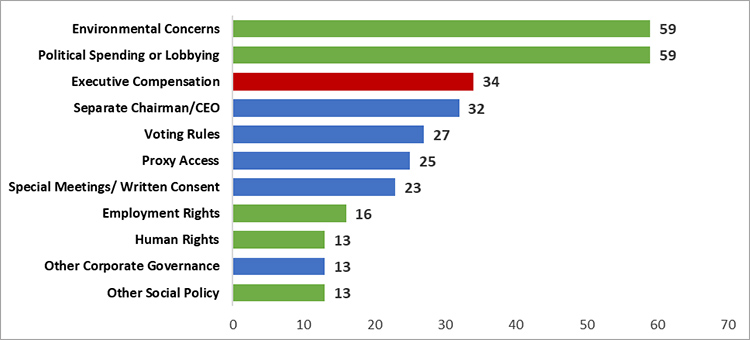

In 2017, to date, environment-related shareholder proposals were a plurality—almost 20%—of all shareholder proposals (Figure 2). This is in keeping with recent trends; in 2016, environment-related shareholder proposals and those involving corporate political spending or lobbying (the second-most common class of shareholder proposal to date this year) each constituted 19% of all shareholder proposals introduced (Figure 3).

Figure 2. Shareholder Proposals by Subtype, 2017*

Source: ProxyMonitor.org database

*For 225 of 250 companies with annual meetings scheduled through the end of June

Figure 3. Shareholder Proposals by Subtype, 2016

Source: ProxyMonitor.org database

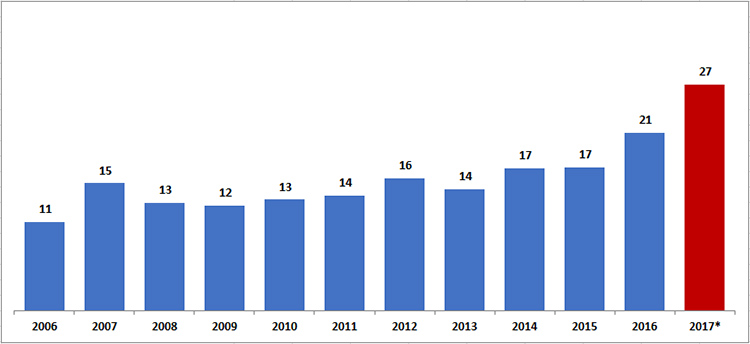

Driven by increased support for shareholder proposals seeking a company report on the “portfolio risk” of the Paris Agreement’s “Two-Degrees Celsius” scenario, the average percentage shareholder support for environment-related shareholder proposals increased to 27% in 2017, the highest year on record (Figure 4). Excluding the 12 portfolio-risk proposals, however, overall shareholder support for environment-related shareholder proposals in 2017 was 20%, slightly below shareholder support for all environment-related shareholder proposals in 2016. Among the 12 portfolio-risk proposals, eight failed to garner majority shareholder support. The 12th, at Chevron, was withdrawn. Given the significant likelihood that this class of proposals may now win a backing of a majority of shareholders, we may see more negotiated withdrawals of such proposals in the future.

Figure 4. Average Percentage Vote for Environment-Related Shareholder Proposals

Source: ProxyMonitor.org database

*In 2017, for 225 of 250 companies with annual meetings scheduled through the end of June

Voting on environment-related shareholder proposals is bifurcated. Certain classes of proposals that are generally supported by the proxy advisory firms,[9] Institutional Shareholder Services and Glass Lewis, received on average between 23% and 42% shareholder support—with significantly lower support when one or both proxy advisors departed from their general support.[10] Among these are proposals asking companies to prepare reports on greenhouse gas emissions, methane emissions, product packaging, carbon-asset risk, environmental and human-rights risks, and “sustainability.”[11] Other proposals typically received 20% or less shareholder support, including those seeking to nominate an independent director with environmental expertise or to link executive pay to “sustainability metrics.” Several idiosyncratic environment-related shareholder proposals were opposed by more than 90% of shareholders. A proposal by the Nebraska Peace Foundation on the proxy ballot for Berkshire Hathaway, asking the company to divest its fossil-fuel-related holdings, was opposed by almost 99% of shareholders.

Discussion

In recent years, regulators and activists have placed renewed emphasis on environmental risks for companies. In 2010, the SEC adopted new guidelines requiring publicly traded corporations to make new disclosures related to “climate risks.”[12] In November 2015, New York attorney general Eric Schneiderman announced an investigation of ExxonMobil over its funding of research related to climate change, an effort later joined by then–California attorney general Kamala Harris and other state and regional government attorneys.[13] In July 2016, the founder and president of a group called the Sustainability Accounting Standards Board—a riff on that of the Financial Accounting Standards Board, the private nonprofit organization that the SEC has designated to set generally accepted accounting principles since 1973—sent a letter to the SEC arguing for the inclusion of criteria for environmental, social, and governance (“ESG”) concerns in the list of financial metrics required in publicly traded companies’ agency-mandated disclosures.[14]

Although the risks from climate change per se are too far in the future to be relevant for assessing a company’s share value, the legislative and regulatory risks involving climate change can be very real; such risks are the best rationale for the SEC’s climate-change disclosure guidelines, as this finding’s lead author has previously discussed.[15] What is harder to explain, from a share-value perspective, is why large institutional shareholders would have been so much more likely to support a substantially identical shareholder proposal concerning the “portfolio risk” stemming from the Paris Agreement in 2017, as compared with 2016. These proposals received more than 62% support at ExxonMobil and more than 65% at Occidental this year, as opposed to 38% and 41%, respectively, in 2016.

The Paris Agreement was entered into in fall 2015, so it was known to institutional investors in the 2016 proxy season. Institutional investors’ voting shift was not caused by a change in approach from the proxy advisory firms, which have not changed their general support for such proposals. And the broadly unanticipated results of the fall 2016 presidential election in the United States would logically be expected to lower climate-change policy risks for energy companies, given President Trump’s greater skepticism of climate-change-related regulations;[16] indeed, on June 1, the president announced that the United States would be pulling out of the Paris Agreement.[17]

Five hypotheses might explain institutional investors’ shift.

First, notwithstanding that the Paris Agreement was adopted in late 2015, institutional inertia may have prevented them from a full analysis of the issue in advance of the 2016 proxy season, which ended in mid-June of that year. Perhaps, on further assessment, institutional investors changed their perspective.

Second, the Department of Labor promulgated Interpretive Bulletin 2015-01 in October 2015, which broadened the fiduciary scope for private pension plans to embrace ESG criteria in voting their investment holdings.[18] Although managers of pension funds governed by the Employee Retirement Income Security Act (ERISA)[19] could have taken advantage of these new rules in the 2016 proxy season, they may have modified their voting rules the following year, after more time to consider their voting policies.

Third, asset managers who make decisions on whether to buy or sell securities are generally not involved in setting institutional investors’ voting policies. Instead, larger institutional investors that develop voting guidelines and decisions for fund families have in-house corporate-governance teams that are often staffed by former employees of proxy advisors.[20] These corporate-governance teams may have changed in composition or changed their opinions among themselves or in conversation with proxy advisors, without carefully considering the reduced climate-change-related portfolio risks in 2017, relative to the prior year.

Fourth, although institutional investors are generally charged with fiduciary duties to vote their shares consistent with shareholder value,[21] individuals setting voting policies for institutional investors are human, and their personal policy preferences may seep into their judgment. The Paris Agreement does create some policy risks for global companies. And although those risks were lower year-over-year after the election, individuals supportive of the Obama administration’s regulatory agenda in this space—and hostile to the agenda of the Trump administration—may have shifted their voting recommendations in response to the election, notwithstanding a lesser basis for portfolio-risk concerns.

A fifth explanation may be somewhat more concerning—and bears watching, as it may have spillover effects into other areas in which institutional investors respond to shareholder activists’ campaigns. In exercising their voting duties as fiduciaries, institutional investors governed by ERISA or operating under a share-value-maximization norm should be supporting the average shareholder’s interests. Even if some shareholders support environmental issues, animal rights, human rights, or other non-pecuniary concerns, most shareholders’ interests as investors are aligned around maximizing their investment returns.[22]

Institutional investors that lack captive capital, however—like most large mutual-fund families—have an economic self-interest that is predicated principally on assets under management. Simply put, more dollars invested in institutional investors’ funds means more money for asset-management firms. Thus, such institutional investors, at least in theory, may be sensitive to marginal investors’ preferences, given that a sustained and successful effort to divest from a large mutual-fund family could cause a drop in the funds’ assets under management. To be sure, assets under management will also be highly sensitive to investment returns. But if an institutional investor decides that a socially oriented shareholder proposal—such as the proposed portfolio-risk report—has some negative cost to company returns but not sufficiently so as to harm materially overall portfolio returns, it may decide to support the proposal in the face of public pressure. Even if the fund family deemed the negative cost to be material, it would be conflicted if the cost was outweighed by the prospects of higher lost assets under management in the face of public pressures. This is particularly true if other institutional investors are making parallel choices—as a divestment-style campaign against an institutional investor would be much more likely to have an impact if a fund was an outlier among its peers.

There is significant evidence that at least some institutional investors did respond to social-investing activists’ pressures by modifying their investment policies. In March, BlackRock committed itself to “prioritize talking with companies on climate risk, gender balance on boards and other long-term strategic issues, and vote against their directors when it feels the companies are not acting.”[23] BlackRock’s new commitment to such engagement was prompted by a proposal introduced by Walden Asset Management and other social-investing and public-pension investors for the investment firm’s own May 2017 annual meeting.[24] Reportedly, the social investors’ “move was partly motivated by frustration [that] BlackRock and some other large shareholders like Vanguard . . . declined to support a single shareholder proposal on board diversity or climate change in 2016.”[25] Walden and other investors made similar pushes at JPMorgan Chase, Bank of New York Mellon, T. Rowe Price, and Vanguard.

Outlook

The shift in institutional investors’ support for climate-change-related shareholder proposals in 2017 may augur a paradigm shift in the shareholder-engagement process—as activists target institutional investors themselves as a tactic through which they hope to influence corporate behavior. Institutional investors may be less sensitive to the full panoply of social-investing concerns, beyond climate change and gender, but these trends deserve careful attention in the future.

ENDNOTES

- Under the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010, publicly traded companies must hold shareholder-advisory votes on executive compensation annually, biennially, or triennially, at shareholders’ discretion. See Pub. L. No. 111-203, 124 Stat. 1376, § 951 (2010).

- See Proxy Monitor, Reports and Findings.

- Although corporate governance in the U.S. is mostly governed by substantive state law, cf. Del. Code Ann., tit. 8, § 211(b) (2009) (noting that, in addition to the election of directors, “any other proper business may be transacted at the annual meeting”); the federal SEC controls the process of proxy solicitation under rules promulgated under section 14(a) of the Securities and Exchange Act of 1934, 4, Pub. L. No. 73-291, ch. 404, 48 Stat. 881 (1934).

- See 17 C.F.R. § 240.14a-8 (2007).

- In a 1945 opinion release, the director of the SEC’s division of corporate finance explained that the shareholder-proposal rules were not intended “to permit stockholders to obtain the consensus of other stockholders with respect to matters which are of a general political, social or economic nature.” Securities Exchange Act Release No. 3638 (Jan. 3, 1945), 11 Fed. Reg. 10,995 (1946). In 1970, the U.S. Court of Appeals for the D.C. Circuit remanded to the SEC for further consideration a 1969 no-action letter by the SEC staff that had applied this rule in advising Dow Chemical that it could exclude a shareholder proposal from the Medical Committee on Human Rights asking that the company cease manufacturing napalm. See Med. Comm. for Human Rights v. Sec. & Exch. Comm’n, 432 F.2d 659, 663 (D.C. Cir. 1970), vacated as moot, 404 U.S. 403 (1972). In 1972, the SEC narrowed its earlier interpretation to apply only to shareholder proposals “not significantly related to the business of the issuer or not within its control.” Exchange Act Release No. 9784, 37 Fed. Reg. 23,178, 23,180 (1972). In 1976, the SEC issued an interpretive release stating that shareholder proposals related to the “ordinary business” of the corporation could only be invoked to exclude proposals that “involve business matters that are mundane in nature and do not involve any substantial policy or other considerations”—essentially inverting the prior rule. Adoption of Amendments Relating to Proposals by Security Holders, Exchange Act Release No. 12,999, 41 Fed. Reg. 52,994, 52,997–98 (1976).

- See Liam Kennedy, Top 400 Asset Managers 2016: Global Assets Now €56.3trn, INVESTMENT & PENSIONS EUROPE (June 2016).

- See BlackRock, Our Engagement Priorities for 2017–2018.

- Emily Chasan, BlackRock Finds Shareholder Action Goes Both Ways, BLOOMBERG BRIEFS, Mar. 16, 2017.

- See ISS, 2016 United States Summary Proxy Voting Guidelines 60 (Dec. 18, 2015).

- As explored in a 2012 Manhattan Institute Proxy Monitor report, an ISS recommendation that shareholders vote “for” a given shareholder proposal tends to correspond with a 15-percentage-point increase in the shareholder vote for the proposal, controlling for other factors. See James R. Copland et al., Proxy Monitor 2012: A Report on Corporate Governance and Shareholder Activism 20–23 (Manhattan Inst. for Pol’y Res., Fall 2012). Support from other proxy advisory firms, including Glass Lewis, doubtless leads to additional increases in the shareholder vote. “Smaller institutional investors, who are more likely to ‘follow’ ISS, place little value on shareholder voting rights themselves—they gain little value from voting ‘better,’ as the broader voter-ignorance literature would suggest.” See id. at 23 (citing Bryan Caplan, THE MYTH OF THE RATIONAL VOTER (2007)). ISS has generally been much more supportive of environmental proposals than the median shareholder, and it has increased the range of proposals that it has been willing to support over time. For example, from 2006 through 2009, ISS generally recommended a vote against “proposals that call for reduction in greenhouse gas emissions by specified amounts.” See, e.g., RiskMetrics Group, 2009 U.S. Proxy Voting Guidelines Summary 55 (Dec. 24, 2008). For the 2010 proxy season and thereafter, ISS generally recommended a vote for “shareholder proposals calling for the reduction of GHG or adoption of GHG goals in products and operations.” See, e.g., RiskMetrics Group, 2010 SRI U.S. Proxy Voting Guidelines 68 (Jan. 2010). Given its business incentives, it is unsurprising that ISS’s recommendations are “systematically biased in favor of shareholder-proposal activism”; “ISS receives significant revenues from social investment vehicles and labor-union pension funds, which gives the company an incentive to favor ‘socially responsible’ investing proposals.” Copland et al., supra, at 23.

- “Sustainability” is a catch-all environmental concept broadly defined as “creat[ing] and maintain[ing] the conditions under which humans and nature can exist in productive harmony to support present and future generations.” U.S. Environmental Protection Agency, Learn About Sustainability.

- See Commission Guidance Regarding Disclosure Related to Climate Change, Exchange Act Release No. 34-61469, 75 Fed. Reg. 6290, 6291, 6296; John M. Broder, S.E.C. Adds Climate Risk to Disclosure List, N.Y. TIMES, Jan. 27, 2010, at B1.

- See John Schwartz, State Officials Investigated over Their Inquiry into Exxon Mobil’s Climate Change Research, N.Y. TIMES, May 19, 2016.

- See Howard Husock & James R. Copland, “Sustainability Standards” Open a Pandora’s Box of Politically Correct Accounting, INVESTOR’S BUSINESS DAILY, Mar. 24, 2017.

- See James R. Copland, Against an SEC-Mandated Rule on Political Spending Disclosure: A Reply to Bebchuk and Jackson, 3 HARV. BUS. L. REV. 381, 398 n. 66 (2013) (“[E]ven if the costs imposed by climate change risks per se would be minimal to shareholders, given reasonable stock-market discount-rate assumptions, the legislative and regulatory risks related to climate change concerns could be quite significant to many businesses. Thus, a mandatory disclosure rule related to climate change, unlike that for political spending, would seem to meet a basic materiality threshold”).

- See Erica Goode, What Are Donald Trump’s Views on Climate Change? Some Clues Emerge, N.Y. TIMES, May 20, 2016, at A11.

- See David Francis, Trump Pulls Out of the Paris Climate Agreement, FOR. POL’Y, June 1, 2017.

- See Interpretive Bulletin Relating to the Fiduciary Standard Under ERISA in Considering Economically Targeted Investments.

- See 29 U.S.C. § 1003.

- Smaller institutional investors, in contrast to their larger brethren, largely outsource their votes to proxy advisory firms. As discussed, proxy advisors’ position on these issues is generally more activist and more supportive of social investing than the median shareholder’s, and proxy advisors’ positions have not changed year-over-year, which means that proxy advisory firms’ policy guidelines cannot explain the shift in institutional-investor voting sentiment.

- There are exceptions, including funds operating with an express social-investing purpose. Even for retirement plans, religious organizations’ pensions and those under the auspices of state and municipal governments are exempt from federal ERISA requirements. See 29 U.S.C. § 1003(b).

- See U.S. Chamber of Commerce Center for Capital Markets Competitiveness, Essential Information:

Modernizing Our Corporate Disclosure System (Winter 2017), at 8 (“[A]n investor that bases its voting and investment decisions on promoting social or political goals is not a reasonable investor for purposes of determining the materiality of information under the federal securities laws, even if that investor’s perspective is rational, sensible, and sound when it comes to that investor’s non-financial motivations”).

- Chasan, supra note 8. See BlackRock, supra note 7.

- See Chasan, supra note 8.

- Id.