PROXY MONITOR 2015

FINDING 4

2015 Proxy Season Wrap-Up

More shareholder proposals introduced and received majority support than in any year since 2010; New York City pensions’ proxy-access push mostly successful

By James R. Copland

ABOUT PROXY MONITOR

The Manhattan Institute’s ProxyMonitor.org database, launched in 2011, is the first publicly available database cataloging shareholder proposals and Dodd-Frank-mandated executive advisory votes[1] at America’s largest companies. The sortable, searchable database includes the nation’s 250 largest companies by revenues, as listed by Fortune.[2] This is the 34th publication in a series of findings and reports by Manhattan Institute Center for Legal Policy director James R. Copland, each drawing upon information in the database to examine shareholder activism in which investors attempt to influence corporate management through the shareholder-proposal process.[3]

|

The 2015 “proxy season”—when corporate America holds annual meetings to vote on company business—is now complete. 216 of the 250 largest U.S. companies, by revenues, have held their annual meetings. Two more are calendared for July; the remainder will meet later in the year.

Among the company business considered at annual meetings, shareholders vote on their own proposals: resolutions that any long-term owners of at least $2,000 of equity securities may introduce on a company’s proxy statement, under rules promulgated by the federal Securities and Exchange Commission (SEC),[4] subject to substantive state law. The story of the 2015 proxy season, at least with regard to this shareholder-proposal process, is New York City Comptroller Scott Stringer’s widespread, successful campaign for a corporate “proxy access” rule. Such a rule would grant shareholders, given ownership and holding-period requirements, the power to nominate directors to the board on the company’s proxy statement. Comptroller Stringer initiated this effort, part of what he calls his Boardroom Accountability Project,[5] through his role as the managing fiduciary of the pension funds for New York City public employees.[6]

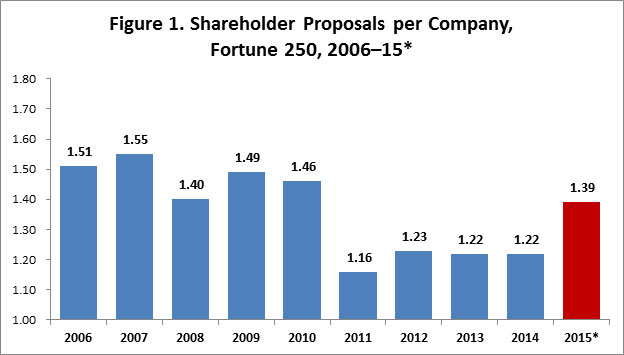

Proxy-access proposals have constituted 11 percent of all shareholder proposals introduced at large companies this year, more than any other class of shareholder proposal save those involving the environment, corporate political spending or lobbying, or separating the company’s chairman and chief executive officer (CEO) roles. The mass introduction of proxy-access proposals is responsible for an uptick in overall shareholder-proposal activity in 2015: the average Fortune 250 company faced 1.39 shareholder proposals in 2015, the most since 2010 (Figure 1). (In 2010, Congress passed the Dodd-Frank financial reform legislation,[7] which obviated shareholder proposals seeking advisory voting rights on executive compensation packages by mandating that publicly traded U.S. companies hold such votes on an annual, biennial, or triennial basis.)

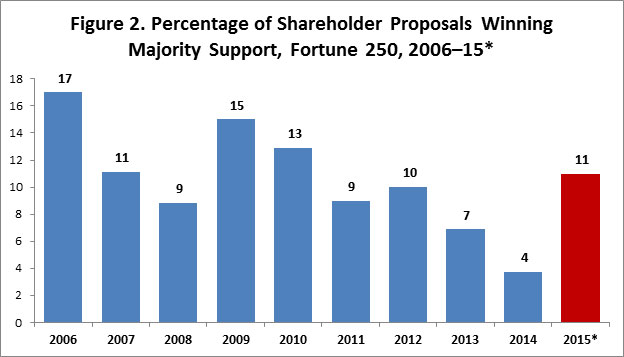

A majority of shareholders supported 23 of the 34 proxy-access proposals introduced in 2015 (68 percent)—as compared to only nine of 272 proposals relating to any other topic. As such, 11 percent of shareholder proposals received majority votes, the highest percentage since 2010 (Figure 2). Absent proxy-access proposals, however, only three percent of shareholder proposals received majority shareholder support, a smaller percentage than in any other year among the last ten (the totality of all years comprising the ProxyMonitor.org database).

Section I examines 2015 shareholder-proposal activity more granularly, answering: (1) who introduced shareholder proposals; (2) what subject matters shareholder proposals involved; and (3) when shareholder proposals were likely to receive shareholder support. Section II looks at proxy-access proposals more specifically, both those introduced by the New York City pension funds and those introduced by other shareholders, examining where such proposals were introduced and why the companies facing such proposals were targeted.

*218 of 250 companies had filed proxy documents by June 30, 2015.

*216 of 250 companies had held annual meetings by June 30, 2015.

I. Shareholder Proposal Filings: The Who, What, and When

(1) Who: Shareholder Proposal Sponsors

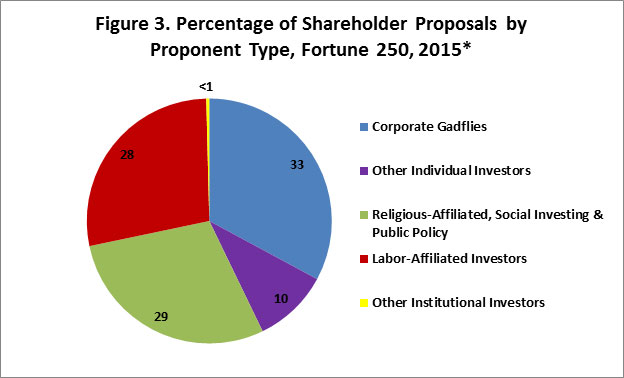

As has been the case in each of the last ten years covered in the ProxyMonitor.org database, the overwhelming majority of shareholder proposals were sponsored by a small group of shareholders (Figure 3):

- Corporate gadflies—a handful of individuals and their family members who repeatedly file common shareholder proposals at multiple companies (33 percent)[8]

- Social investors—institutional investors with a social, religious, or policy purpose (29 percent)[9]

- Labor-affiliated investors—pension funds affiliated with labor unions or public employees (28 percent)[10]

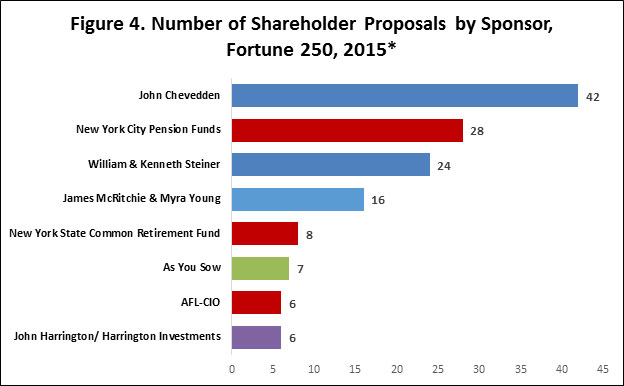

Although the definition of who might be deemed a corporate gadfly may vary, three individuals and their family members—John Chevedden, the father-son team of William and Kenneth Steiner, and the husband-wife team of James McRitchie and Myra Young—have been particularly active. These gadfly investors were three of the four most-active sponsors of shareholder proposals in 2015 (Figure 4), collectively sponsoring about one-third of all shareholder proposals this year.

Among social investors, only As You Sow introduced more than five proposals in 2015 (seven). Many other socially oriented investors sponsored multiple proposals, however: social-investing platforms Arjuna Capital (three), Domini Social Investments (three), Green Century Capital Management (three), Investor Voice (five), Northstar Asset Management (two), Trillium Asset Management (four), and Walden Asset Management (four); religious investors Congregation of Sisters of St. Agnes (two), Sisters of Mercy (five), Province of St. Joseph of the Capuchin Order (two), Sisters of St. Dominic (two), Sisters of St. Francis (three), and the Unitarian Universalist Association of Congregations (two); the public-policy group National Center for Public Policy Research (two); and the Nathan Cummings (two) and Park (three) charitable foundations.

After John Chevedden, the New York City pension funds have been the second-most-active sponsor of shareholder proposals in 2015. The New York State Common Retirement Fund, which oversees pension assets for most of the Empire State’s state and municipal workers, excluding teachers and those employed by New York City, introduced eight proposals; the multiemployer pension plan for the American Federation of Labor-Congress of Industrial Organizations (AFL-CIO) sponsored six. Other labor-affiliated investors introducing multiple shareholder proposals in 2015 were the Philadelphia Public Employee Retirement System (four) and the multiemployer pension plans for the American Federation of State, County, and Municipal Employees (AFSCME) (two), Change to Win (CtW) (three), the International Brotherhood of Electrical Workers (four), the International Brotherhood of Teamsters (two), and the United Automobile Workers (UAW) (four).

Individuals other than the three most-active corporate gadflies introduced ten percent of all 2015 shareholder proposals, though many of these are repeat filers who might also be considered gadflies, including Gerald Armstrong and John Harrington (who also sponsors proposals through his social-investment fund, Harrington Investments).[11] Only a single shareholder proposal was sponsored by an institutional investor without a labor affiliation or social, policy, or religious purpose—a proposal by activist investor Nathan Peltz’s Trian Fund Management at DuPont, related to his ultimately unsuccessful effort to take four board seats and break up the company.[12]

*218 of 250 companies had filed proxy documents by June 30, 2015.

*218 of 250 companies had filed proxy documents by June 30, 2015.

(2) What: Shareholder Proposal Types

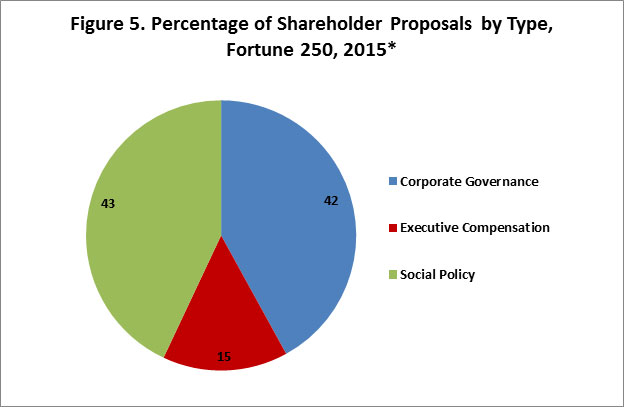

As was the case in 2006–14, shareholder proposals relating to social or policy concerns constituted a plurality of all such proposals in 2015 (43 percent) (Figure 5). Close behind were proposals relating to corporate-governance issues (42 percent), buoyed by Comptroller Stringer’s proxy-access campaign. 15 percent of all shareholder proposals involved executive compensation.

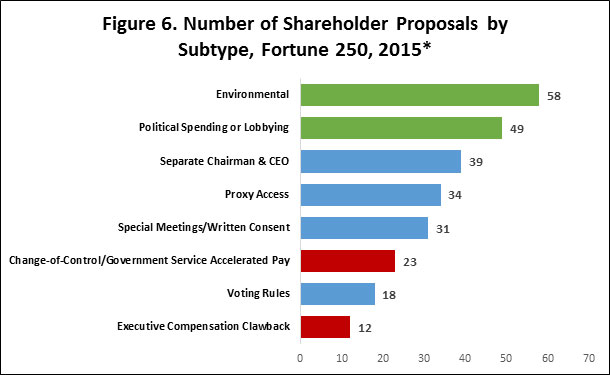

As for subclasses of proposal, environmental concerns were introduced most often in 2015 (58 proposals) (Figure 6). Proposals related to political spending or lobbying—the most-introduced subclass in 2012, 2013, and 2014—were the second-most numerous (49 proposals). Most corporate-governance proposals involved separating the chairman and CEO roles (39), proxy access (34), empowering shareholders to call special meetings or act through written consent (31), or voting rules (18). Shareholder proposals related to executive compensation tended to concern accelerated executive pay in the event of a change in corporate control or an executive moving to a government job (23) or “clawbacks” for previously awarded pay in the event of an adverse government action affecting the company (12). Collectively, these eight subjects comprised 86 percent of all shareholder proposals introduced in 2015.

*218 of 250 companies had filed proxy documents by June 30, 2015.

*218 of 250 companies had filed proxy documents by June 30, 2015.

(3) When: Shareholder Proposal Voting by Proposal Subtype

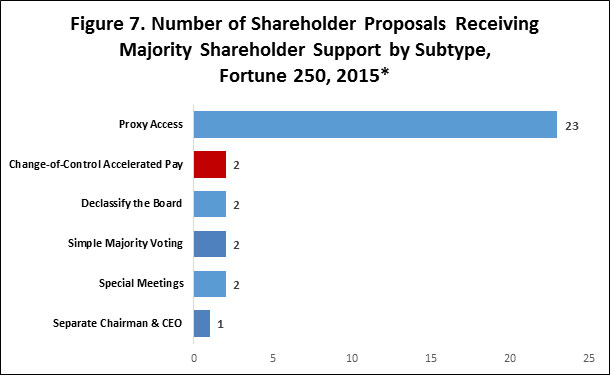

In 2015, shareholder proposal voting was largely a bifurcated tale: 23 of 34 proxy-access proposals received majority shareholder support (68 percent), including 19 of the 23 such proposals introduced by the New York City pension funds (83 percent) (Figure 7). Only nine other shareholder proposals received majority support:

- Two of 23 shareholder proposals involving executives’ accelerated pay in the event of a change in corporate control or the executive’s entry into government service

- Two of two proposals seeking to “declassify” the company’s board (i.e., to elect all directors annually instead of in staggered, overlapping terms—premised on the notion that staggered board terms are an impediment to prospective takeover bids that may benefit shareholders)[13]

- Two of 18 shareholder proposals involving shareholder voting rules (each seeking to eliminate supermajority voting requirements from company bylaws)

- Two of 31 proposals seeking to allow shareholders to call special meetings or act through written consent (each involving special-meeting rights)

- One of 39 shareholder proposals seeking to separate the company’s chairman and CEO roles (introduced by John Chevedden at the media company Omnicom, which currently separates the two positions)[14]

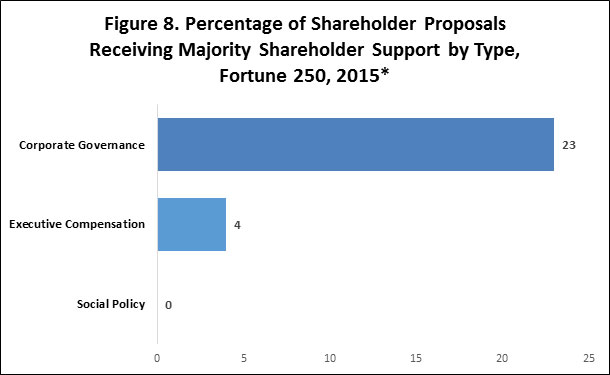

Overall, 23 percent of shareholder proposals involving corporate-governance concerns received majority shareholder support (Figure 8), although this percentage is highly skewed by the success of proxy-access proposals. Excluding proxy-access proposals, only seven percent of corporate-governance-related shareholder proposals received majority shareholder backing. Just four percent of shareholder proposals related to executive compensation were supported by a majority of shareholder proposals. No shareholder proposals related to social or policy issues received majority support—in keeping with each of the nine prior years in the ProxyMonitor.org database, when not a single social-policy-related shareholder proposal has received the support of a majority of shareholders over board opposition.

*216 of 250 companies had held annual meetings by June 30, 2015.

*216 of 250 companies had held annual meetings by June 30, 2015.

II. Proxy-Access Proposals: The Where and Why

New York City Comptroller Scott Stringer’s campaign for proxy access, if judged by shareholder voting results, has been an unqualified success: 19 of the 23 proxy access proposals sponsored by the New York City pension funds at Fortune 250 companies received the support of a majority of shareholders. The exceptions each saw more than 40 percent of shareholders vote in favor of the proposal: energy giant ExxonMobil (49.4 percent), auto-parts manufacturer PACCAR (42 percent), and electricity companies Exelon (43 percent) and Southern (46 percent). (Exelon introduced its own proxy access proposal, which received majority shareholder support.)

Of course, success in shareholder voting results is only the first step in analyzing the push for proxy access. Ultimately, these proposals are premised on the notion that lowering the barriers to entry for large, diversified shareholders to nominate directors competing with those tapped by board nominating committees would increase shareholder value. Indeed, the press release touting the New York City pension funds’ proxy access claims that the proposed rule could “raise the market cap of publicly held companies in the United States by up to $140 billion, or 1.1 percent,”[15] citing research by the CFA Institute.[16] Such claims are not, however, universally accepted.

In 2011, when the U.S. Court of Appeals for the D.C. Circuit threw out the SEC’s promulgated mandatory proxy-access rule, which was substantially similar to that proposed by the New York City funds, it cited concerns that “unions and state and local governments whose interests in jobs may well be greater than their interest in share value, can be expected to pursue self-interested objectives rather than the goal of maximizing shareholder value.”[17] Notwithstanding the overall success of New York City funds’ push for proxy access, a substantial fraction of shareholders (27–68 percent) have opposed each of these proposals, unless supported by the companies’ boards of directors. (A significantly higher percentage of shareholders supported the proposal at Citigroup, after the board agreed with the proposal.) Included among the investors not supporting the proxy access proposals are the two largest mutual fund groups, Fidelity and Vanguard.[18]

In time, scholars and analysts will assuredly assess the impact of the proxy access proposals’ impact on share value. For now, it is notable that the New York City funds’ methodology in determining which companies to target suggests that the campaign may be related to concerns other than share value. The funds expressly targeted companies based on three criteria: “climate change, board diversity and excessive CEO pay.”[19] Of these, executive pay is plausibly related to share value to the extent that excessive pay may dilute share ownership and otherwise serve as a proxy for agency costs (management insensitivity to shareholder interests).[20] Moreover, rather than attempting to reach an independent determination of appropriate pay, the New York City funds relied on negative shareholder sentiment as expressed in the prior year’s shareholder advisory vote on executive compensation—a vote that may be significantly influenced by proxy advisory firms but nevertheless is a defensible “bottom-up” methodology for identifying companies at which shareholders have expressed pay concerns.

However, the other two “priority issues” used to select target companies for Comptroller Stringer’s proxy access campaign[21] have attenuated, if any, connections to share value. Although “diversity” in the boardroom has become a hot topic in corporate-governance circles[22]—chiefly focusing not on business experience but sex, race, or ethnicity—empirical scholarship supporting the notion that board diversity matters for shareholder value is mixed at best, with several studies showing that gender diversity is negatively associated with share value, particularly when required or pressed by government mandate.[23]

As observed by Duke law professor Kimberly Krawiec, the business case for or against board diversity remains unproven.[24] Board diversity may confer a theoretical benefit to share value, if an attenuated and empirically unproven one, but it is difficult to conceive of any rationale in which proxy access would make particular sense for “carbon-intensive coal, oil and gas, and utility companies,”[25] the principal target of Stringer’s campaign. To be sure, such companies may face peculiar regulatory risks, if rather obvious for energy and utility companies and their investors. (The risks that climate change itself may place on such companies’ business models are too far in the future—and thus too discounted to present—to concern shareholders focused solely on share price, aside from sociopolitical or regulatory concerns.[26]) Yet beyond changing their line of business or increasing lobbying or political activity, there is little that such companies can do to mitigate such risks—and the former (but not the latter)[27] would almost certainly be inimical to share value.

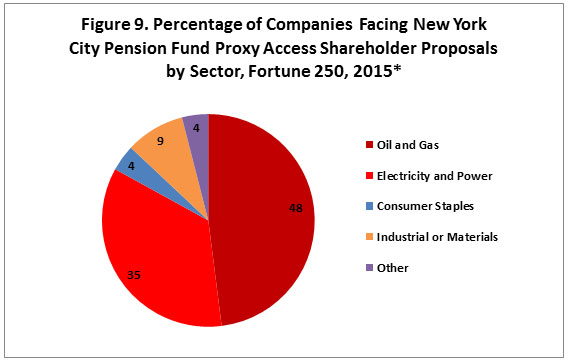

Four of the five largest companies facing proxy-access proposals from the funds, via the Boardroom Accountability Project, were in the oil and gas sector,[28] as were 48 percent of the companies in the ProxyMonitor.org database facing proxy-access proposals sponsored by the New York City pension funds; another 35 percent were electric-utility companies. In total, 83 percent of the largest companies targeted by the New York City funds were in the energy or electric space.

*218 of 250 companies had filed proxy documents by June 30, 2015.

The New York City pension funds may have targeted energy and electric companies with proxy access proposals using a blunderbuss approach, but their campaign has the virtues of clearly defined criteria and transparency. There is no evidence that Comptroller Stringer was targeting particular companies with self-interested objectives beyond the three priority issues the campaign publicly identified. In contrast, the other labor-affiliated investors sponsoring proxy access proposals in 2015—one each among CalPERS, the Connecticut Retirement Plans and Trust Funds, the CtW Investment Group, and the UAW Retiree Medical Benefits Trust—may have selected their targets with an eye toward influencing the companies for union-related, not investment-related, reasons. These funds’ targets—Community Health Systems, Kohl’s, McDonald’s, and Walgreens Boots Alliance—have each been in the crosshairs of ongoing wage and union-organizing campaigns:

- Community Health, the largest non-urban provider of hospital healthcare, has been involved in contentious litigation with labor over efforts to unionize registered nurses.[29]

- Kohl’s, one of the largest U.S. retailers, has been facing specific union agitation over wages and labor conditions, including at the company’s annual meeting.[30]

- McDonald’s, the nation’s largest fast-food employer, has been the principal target of union organizers’ “Fight for 15” campaign, aimed at dramatically increasing fast-food workers’ wages.[31]

- Walgreens, the nation’s largest drug retailer, has emerged as a principal target of labor wage campaigns, which were previously successful in pressuring retailers like WalMart and Target to increase payscales.[32]

Beyond these general labor-oriented issues, the sponsor of the proxy access proposal at Kohl’s, CalPERS, may have other self-interested reasons to focus on the company. CalPERS is the principal creditor in the bankruptcy of Golden State municipality San Bernardino,[33] and it has been aggressively pursuing its interests at the expense of other bondholders;[34] Kohl’s is San Bernardino’s largest outside creditor, owed $29.4 million at the time of the city’s bankruptcy.[35]

Though it is certainly possible that the non-New York City labor-affiliated funds targeted these four particular companies with proxy access proposals for objectively neutral reasons, the fact that targeted companies were so central to union campaigns (and, in CalPERS’s case, the sponsor’s own self-interest) raises a red flag. It is possible that the sponsoring investors selected such companies to increase their leverage in ongoing disputes—disputes that, were the companies to capitulate to labor’s demands, would harm rather than help diversified shareholders. A majority of shareholders voted for these proposals at Kohl’s and McDonald’s; these companies’ responses—and these investors’ future shareholder proposal efforts—warrant close scrutiny.

ENDNOTES

- Under the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010, publicly traded companies must hold shareholder advisory votes on executive compensation annually, biennially, or triennially, at shareholders’ discretion. See Pub. L. No. 111-203, 124 Stat. 1376, § 951 (2010) [hereinafter “Dodd-Frank”].

- See Fortune 500, available at http://fortune.com/fortune500/ (last visited July 8, 2015).

- See Proxy Monitor, Reports and Findings, http://proxymonitor.org/Forms/reports_findings.aspx (last visited July 8, 2015).

- See 17 C.F.R. § 240.14a-8 (2007) [hereinafter 14a-8]. The federal Securities and Exchange Commission determines the procedural appropriateness of a shareholder proposal for inclusion on a corporation’s proxy ballot, pursuant to the Securities Exchange Act of 1934, Pub. L. No. 73-291, Ch. 404, 48 Stat. 881 (1934) (codified at 15 U.S.C. §§ 78a–78oo (2006 & Supp. II 2009)), at §§ 78m, 78n & 78u; 15 U.S.C. §§ 80a-1 to 80a-64 (2000) (pursuant to Investment Company Act of 1940, Pub. L. No. 76-768, 54 Stat. 841(1940)); but the substantive rights governing such measures and how they can force boards to act remain largely a question of state corporate law; cf. Del. Code Ann., tit. 8, § 211(b) (2009) (noting that in addition to the election of directors, “any other proper business may be transacted at the annual meeting”).

- See New York City Comptroller, Boardroom Accountability Project, http://comptroller.nyc.gov/boardroom-accountability/ (last visited Apr. 14, 2015) [hereinafter “Boardroom Accountability Project”]; see also Press Release, Comptroller Stringer, NYC Pensions Funds Launch National Campaign To Give Shareowners A True Voice In How Corporate Boards Are Elected: New York City Pension Funds File 75 Proxy Access Shareowner Proposals to Kick Off the Boardroom Accountability Project, https://comptroller.nyc.gov/newsroom/comptroller-stringer-nyc-pension-funds-launch-national- campaign-to-give-shareowners-a-true-voice-in-how-corporate-boards-are-elected/ [hereinafter “Stringer Press Release”].

- The elected New York City comptroller manages the City’s pension funds, which serve to provide retirement benefits for the City’s public employees. See Office of the State Comptroller, Fiduciary Responsibilities of the Comptroller, http://www.osc.state.ny.us/pension/fiduciary.htm (last visited Sept. 9, 2014). Full fiduciary authority over the funds rests with various boards composed of political and union delegates. For example, the board of the $46 billion Teachers’ Retirement System (TRS) includes the comptroller, two mayoral delegates, a delegate from the education chancellor, and three teacher delegates. See TRSNYC, Our Retirement Board, https://www.trsnyc.org/trsweb/aboutUs/ourRetirementBoard.html (last visited Sept. 9, 2014). The board of the $43 billion New York City Employees’ Retirement System (NYCERS) includes the comptroller, the public advocate, a mayoral representative, each of the five New York City borough presidents, and three union delegates. See NYCERS, Board of Trustees, http://www.nycers.org/(S(azvv04mpy1qd2j5515dyny55))/about/Board.aspx (last visited Sept. 9, 2014).

- See Dodd-Frank, supra note 1, at § 951.

- “Corporate gadflies,” as commonly used in Charles M. Yablon, Overcompensating: The Corporate Lawyer and Executive Pay, 92 Colum. L. Rev. 1867, 1895 (1992); and Jessica Holzer, Firms Try New Tack Against Gadflies, Wall St. J. (June 6, 2011),http://online.wsj.com/article/SB10001424052702304906004576367133865305262.html.

- See Michael Chamberlain, Socially Responsible Investing: What You Need to Know, Forbes (Apr. 24, 2013), http://www.forbes.com/sites/feeonlyplanner/2013/04/24/socially-responsible-investing-what-you-need-to-know (“In general, socially responsible investors are looking to promote concepts and ideals that they feel strongly about.”).

- Pension funds managing retirement assets for employees are among the largest investors in the marketplace and have historically been among the most active sponsors of shareholder proposals at publicly traded corporations. Such funds can be organized for the employees of specific companies or as multiemployer plans affiliated with labor unions that span multiple companies across one or more industries, such as the United Steelworkers, the International Brotherhood of Electrical Workers, AFL-CIO, or AFSCME. Other such funds exist as creatures of states and municipalities on behalf of public-sector workers. These plans are not directly under the control of public-employee labor unions themselves—though, in many cases, the plans vest fiduciary duties with boards peopled in part by union delegates. For instance, the nation’s largest pension fund, that for the California Public Employee Retirement System (CalPERS), has six union delegates on its board in addition to seven officials appointed by elected officials or serving in an ex officio capacity; see CalPERS, Board of Administration, http://www.calpers.ca.gov/index.jsp?bc=/about/board/home.xml (last visited July 8, 2015).

- Harrington Investments describes itself as “a leader in Socially Responsible Investing and Shareholder Advocacy since 1982 ... dedicated to managing portfolios for individuals, foundations, non-profits, and family trusts to maximize financial, social and environmental performance.” Harrington Investments, Inc., About Us, http://harringtoninvestments.com/about-us (last visited Aug. 1, 2014).

- See Liz Hoffman & Timothy W. Martin, Largest U.S. Pensions Divided on Activism, WALL ST. J., May 19, 2015, http://www.wsj.com/articles/largest-u-s-pensions-divided-on-activism-1432075445.

- See, e.g., Lucian A. Bebchuk, Alma Cohen, and Charles C. Y. Wang, “Staggered Boards and the Wealth of Shareholders: Evidence from Two Natural Experiments,” NBER Working Paper 17127 (June 2011), http://www.nber.org/papers/w17127.

- See OmnicomGroup: Our Leadership, http://www.omnicomgroup.com/about/leadership/ (last visited July 8, 2015).

- See Stringer Press Release, supra note 5.

- See CFA Institute: Proxy Access in the United States—Revisiting the Proposed SEC Rule (Aug. 2014), http://www.cfapubs.org/doi/pdf/10.2469/ccb.v2014.n9.1. The CFA Institute is a global association of chartered financial analysts. See generally CFA Institute, https://www.cfainstitute.org/pages/index.aspx.

- Business Roundtable & Chamber of Commerce of the U.S. v. SEC, 647 F.3d 1144, 1152 (D.C. Cir. 2011).

- See Gretchen Morgenson, Mutual Fund Giants Vote to Keep the Insiders In, N.Y. TIMES, May 31, 2015, at BU1, available at http://www.nytimes.com/2015/05/31/business/fund-giants-resist-proxy-access-board-shake-ups.html.

- See Stringer Press Release, supra note 5.

- See generally Lucian A. Bebchuk et al., Managerial Power and Rent Extraction in the Design of Executive Compensation, 69 U. CHI. L. REV. 751, 788–89 (2002) (discussing the “camouflaging” of managerial rent extraction); Lucian A. Bebchuk & Christine Jolls, Managerial Value Diversion and Shareholder Wealth, 15 J.L. ECON. & ORG. 487, 501 (1999) (showing that “within the standard principal-agent framework, permitting value-diversion imposes a cost on shareholders that may reduce ex ante share value”).

- See Stringer Press Release, supra note 5.

- See, for example, a recent on-line symposium on board diversity at The Faulty Lounge, http://www.thefacultylounge.org/board-diversity/ (last visited July 8, 2015).

- See Kimberly D. Krawiec, What Does Corporate Boardroom Diversity Accomplish?, N.Y. TIMES (Room for Debate, Apr. 1, 2015), http://www.nytimes.com/roomfordebate/2015/04/01/the-effect-of-women-on-corporate-boards/what-does-corporate-boardroom-diversity-accomplish (citing studies); Stephen Bainbridge, PROFESSORBAINBRIDGE.COM (MAY 14, 2015), http://www.professorbainbridge.com/professorbainbridgecom/2015/05/gender-diversity-in-the-boardroom.html (citing studies).

- See Krawiec, supra note 23.

- See Stringer Press Release, supra note 5.

- In 2010, the SEC, in a contested 3–2 vote, adopted new climate-change disclosure regulations. See Commission Guidance Regarding Disclosure Related to Climate Change, Exchange Act Release No. 34-61469, 75 Fed. Reg. 6290, 6291, 6296; John M. Broder, S.E.C. Adds Climate Risk to Disclosure List, N.Y. TIMES, Jan. 27, 2010, at B1. Even if the costs imposed by climate change risks per se would be minimal to shareholders, given reasonable stock-market discount-rate assumptions, the legislative and regulatory risks related to climate change concerns could be quite significant to many businesses.

- See Robert J. Shapiro & Douglas Dowson, Corporate Political Spending: Why the New Critics Are Wrong, in Legal Pol’y Rep. 15, 22 (Manhattan Inst. for Pol’y Res. June 2012), http://www.manhattan-institute.org/html/lpr_15.htm (finding that “corporate political activity appears to have a generally positive effect on firm value, as reflected in excess market returns”).

- See Boardroom Accountability Project 2015 Company Focus List, available at http://comptroller.nyc.gov/wp-content/uploads/2014/11/Board-Room-Accountability-2015-Company-List.pdf.

- See Press Release, National Nurses United, U.S. Court of Appeals Issues Scathing Judgment against Big Hospital Chain, Ordering CHS to Repay Union Costs for “Willful” Failure to Bargain with RNs, May 11, 2015, http://www.commondreams.org/newswire/2015/05/11/us-court-appeals-issues-scathing-judgment-against-big-hospital-chain-ordering (last visited July 9, 2015).

- See Kohl’s Refuses to Hear from Workers Who Keep Its Stores Clean, UNION ADVOCATE, May 14, 2015, http://advocate.stpaulunions.org/2015/05/14/kohls-refuses-to-hear-from-workers-who-keep-its-stores-clean/ (last visited July 9, 2015).

- See Fight for $15, http://fightfor15.org/latest-news/ (last visited July 9, 2015).

- See Nandita Bose, After Target Wage Hike, Labor Groups Turn to Drugstore Chains, PHILLY VOICE, Mar. 21, 2015, available at http://www.phillyvoice.com/after-target-wage-hike-labor-groups-eye-drugstores/ (last visited July 9, 2015).

- See Andrew Edwards, Pension Costs Lead San Bernardino’s Debt, [SAN BERNARDINO] SUN NEWS, Aug. 10, 2012, available at http://www.sbsun.com/general-news/20120810/pension-costs-lead-san-bernardinos-debts (last visited July 9, 2015).

- See Steven Church & Romy Varghese, Calpers’ Pension Hammer Forces “Unfair” Bond Ruling by Judge, BLOOMBERG BUSINESS, May 12, 2015, available at http://www.bloomberg.com/news/articles/2015-05-12/calpers-pension-hammer-forces-unfair-bond-ruling-by-judge (last visited July 9, 2015).

- See Edwards, supra note 33.