PROXY MONITOR 2013

FINDING 1

Watching the 2013 Proxy Season

Union Funds Pushing Companies to Separate Chairman and CEO Roles

PRESS RELEASE

ABOUT PROXY MONITOR

The Manhattan Institute’s ProxyMonitor.org database, launched in 2011, is the first publicly available database cataloging shareholder proposals and Dodd-Frank-mandated[1] executive-compensation advisory votes at America’s largest companies. This is the 17th in a series of findings and reports drawing upon information in the database, each of which examines shareholder activism in which investors attempt to influence corporate management through the shareholder voting process.[2]

|

April 15 is not only “Tax Day”[3] but also the launch of “proxy season,” when publicly traded American companies hold annual meetings and shareholders vote on various proposals submitted to them on proxy ballots. Two of the 250 largest public companies by revenues are meeting on April 15 itself (Public Service Enterprise Group and Goodyear), with three more scheduled to meet on April 16 and another three on April 18. Although only 20 of the Fortune 250companies had met as of April 15, 74 are scheduled to meet between April 15 and May 16, based on companies’ filings with the Securities and Exchange Commission (SEC) as of April 4.

In 2013 to date, as in 2012, the most regularly introduced class of shareholder proposals seeks limits on or greater disclosures of corporate political spending and lobbying. The second-most frequently introduced type of proposal, again consistent with 2012, seeks to require companies to have an “independent chairman” separate from the company’s chief executive officer.

This finding summarizes early 2013 trends in shareholder-proposal submission and voting, as well as executive-compensation advisory voting, paying special attention to proposals seeking to split the chairman and CEO roles. The finding also highlights the shareholder proposals of interest on the horizon between now and mid-May, focusing on four classes of proposals of particular interest: splitting the chairman and CEO, political spending and lobbying, board declassification, and proxy access.[4]

Early 2013 Shareholder-Proposal Trends

In 2013, the average company among the 94 Fortune 250 public companies that have filed statements with the SEC to date has, on average, received 1.24 shareholder proposals, up from 1.21 in 2012 and 1.18 in 2011. This modest increase may be the result of sample bias—i.e., companies filing later in the year may report fewer proposals—so it is important to watch filings throughout the proxy season before passing judgment on this early trend. The number of shareholder proposals filed remains below levels seen from 2006 through 2010, when the Dodd-Frank Act mandated regular shareholder advisory votes on executive compensation,[5] thus negating the need for shareholders interested in such voting rights to introduce such proposals.

Shareholder-Proposal Types, 2013

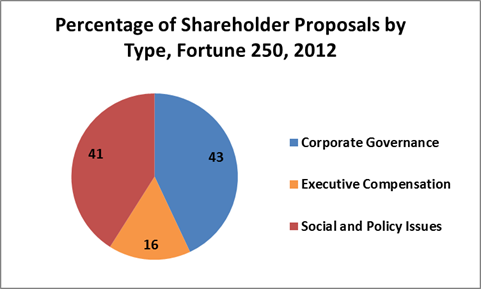

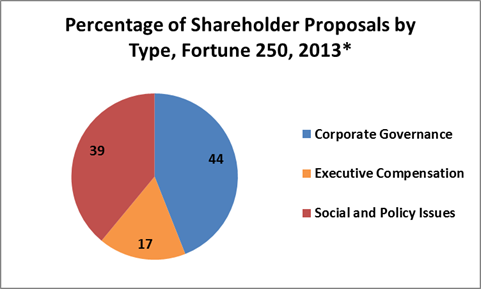

The composition of shareholder proposals in 2013 broadly tracks that seen in 2012. The share of “corporate governance” shareholder proposals (those calling for procedural changes such as modified shareholder voting rules, the elimination of staggered director elections, separating the roles of chairman and chief executive officer, and empowering shareholders to act outside annual meetings by written consent or by calling special meetings) has ticked up slightly (from 43 percent to 44 percent), while the share of proposals related to social and policy issues (involving, e.g., the environment, corporate political spending and lobbying, and human rights) has fallen slightly (from 41 percent to 39 percent).

*To date, 94 companies filed

This modest shift may, however, be largely attributable to sample bias in the early proxy season. Examining the composition of proposals with more granularity, the share of the largest categories of social-policy-related proposals—lobbying and political spending, environmental issues, and human rights—each increased by 2 percentage points in 2013, to date.[6] Therefore, the drop in introduction of social-policy-related proposals is entirely attributable to a decline in other proposal types. Thus far in 2013, not a single proposal related to employment rights and animal rights has been introduced; there were 61 and 58 proposals in these categories, respectively, introduced from 2006 through 2012 at companies in the Proxy Monitor database. Although the number of proposals related to these topics has dropped in recent years, their conspicuous absence to date in 2013 may be merely a function of various companies’ annual-meeting timing, as animal-rights-related proposals, in particular, have typically been introduced at subsets of companies (such as department stores and pharmaceutical companies) in which animal products are sold or animals are tested.[7]

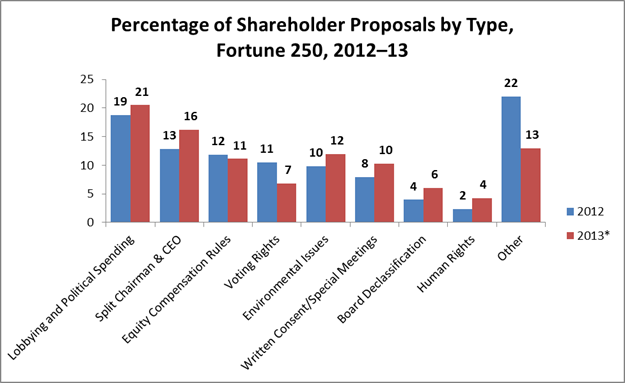

Among shareholder proposals related to corporate governance, the share of proposals related to separating the chairman and CEO (called “chairman independence” by the proponents of this concept), those seeking to empower shareholder action outside annual meetings (through “special meetings” or “written consent”), and those related to electing all directors annually (“board declassification”) has risen in 2013. (The share of board-declassification proposals has increased by 50 percent, under an effort by various public-employee pension funds being coordinated by Harvard law professor Lucian Bebchuk’s Shareholder Rights Project.)[8] The share of proposals related to shareholder voting rights has declined, largely attributable to the absence of “cumulative voting” proposals previously introduced by a single individual “corporate gadfly” shareholder proponent, Evelyn Davis; after scaling back her shareholder activism in 2012,[9] the octogenarian Ms. Davis has filed no shareholder proposals at companies in the Proxy Monitor database in 2013.

*To date, 94 companies filed

*To date, 94 companies filed

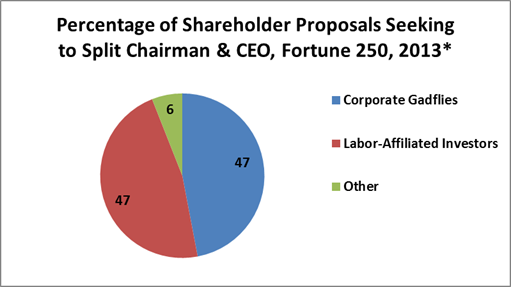

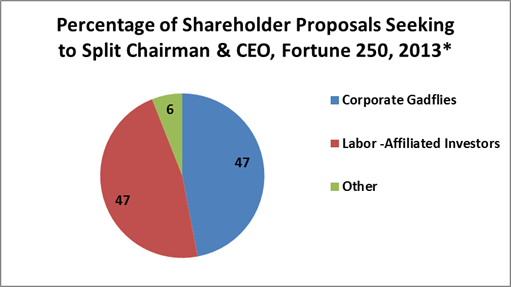

Special Focus: Shareholder Proposals to Split the Chairman and CEO

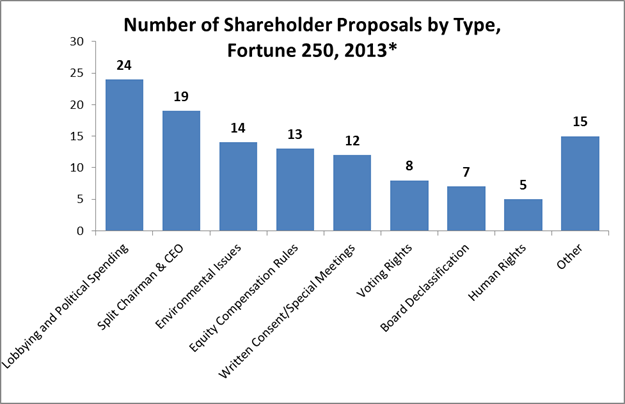

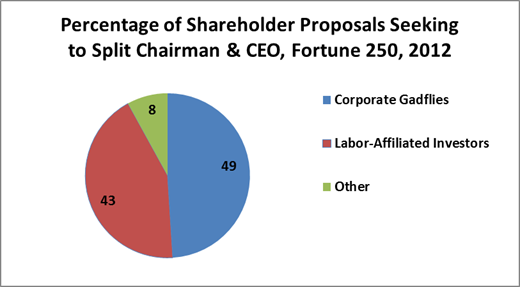

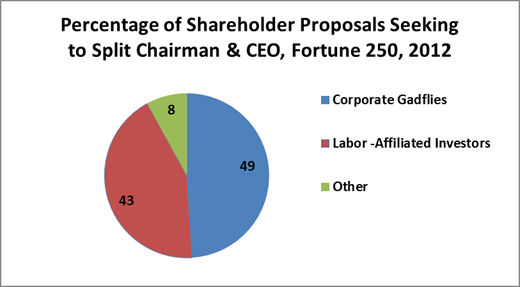

In 2012, the number of shareholder proposals advising companies to separate their chairman and CEO positions more than doubled from the previous year, following an aggressive push on the subject by labor-union funds.[10] As mentioned, such proposals are even more common this year: the share of proposals seeking to separate these functions is up another 23 percent in 2013. That these proposals are the second-most commonly introduced is particularly striking, given that many companies already have a chairman distinct from the CEO. Shareholder activists are clearly making this issue a priority for companies with joint chairman-CEOs.

Proposals to split the roles of chairman and CEO are particularly sensitive for boards and management because, to implement the proposal, the board would, in effect, have to demote the company’s boss (giving him a formal overseer as chairman) or wrest away his day-to-day management of the corporation. A majority vote in favor of such a proposal is thus often viewed as, in essence, a vote of no confidence in corporate management.

The high stakes involved in such proposals may partly explain their particular appeal to investors affiliated with organized labor, which observers from the Department of Labor’s Office of Inspector General to the D.C. Circuit Court of Appeals have worried take a role in shareholder activism to advance labor goals rather than shareholders’ interests:[11] managements seeking to avoid the embarrassment of a shareholder vote to split the chairman and CEO roles may be more willing to negotiate with labor interests to stem off aggressive ballot fights on the issue. As an example of how managements may choose to avoid these proposals, Goldman Sachs recently announced that, for the second straight year, it had negotiated away a proposal to separate its chairman and CEO roles by giving additional powers to its lead independent director.[12] Goldman will be holding its annual meeting in Salt Lake City on May 23.

In both 2012 and 2013, shareholder proposals seeking to separate the chairman and CEO roles have been sponsored overwhelmingly by labor funds and four individual gadfly investors and their family members (John Chevedden, Kenneth and William Steiner, Gerald Armstrong, and James McRitchie). The labor unions sponsoring such proposals over the last two years include the American Federation of Labor–Congress of Industrial Organizations (AFL-CIO), the American Federation of State, County, and Municipal Employees (AFSCME), the Electrical Workers, the Teamsters, the Trowel Trades, the United Auto Workers (UAW), and public-employee pension funds from Indiana, Massachusetts, and New York City.

*To date, 94 companies filed

A recent New York Times article focused on the aggressive push that certain activists are making with such a proposal this year at JP Morgan Chase, scheduled to hold its annual meeting on May 21.[13] Last year, just over 40 percent of shareholders at JP Morgan supported a proposal to split the chairman and CEO roles. Thirteen other companies in the Fortune 250 also saw over 40 percent of their shareholders backing one of these proposals in 2012—including two, McKesson Corporation and Sempra Energy, in which a majority of shareholders supported the proposal. That only two of 39 proposals in 2012 that sought a split chairman-CEO won majority backing shows that most shareholders remain hesitant to dictate “chairman independence” as a one-size-fits-all governance paradigm—perhaps unsurprisingly, since the empirical evidence about whether separation of the chairman and CEO roles adds shareholder value, even on average, is inconclusive.[14] Still, the influential proxy-advisory firm Institutional Shareholder Services (ISS) tends to support these proposals much more often, over two-thirds of the time; and about 14 percent of shareholders tend to follow ISS’s recommendations, when controlling for other factors.[15] Since the average proposal to split these roles won the support of 34 percent of shareholders last year—up from 30 percent from 2006 through 2011—these proposals are ones to watch in 2013.

|

Shareholder-Proposal Sponsors, 2013

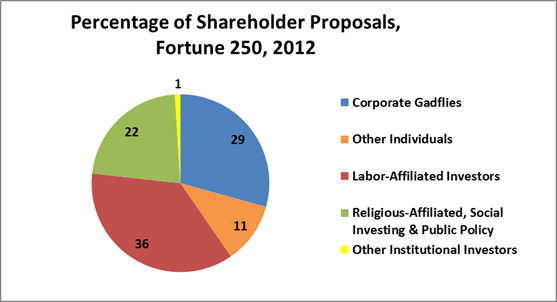

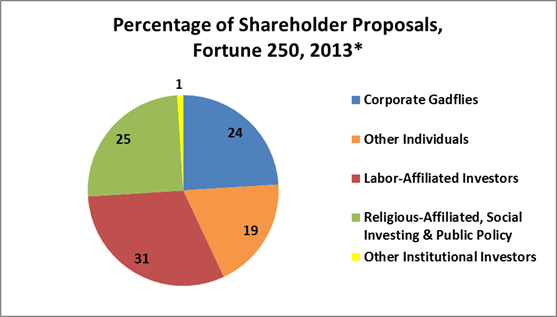

With Ms. Davis’s absence from the shareholder-proposal process in 2013, the percentage of shareholder proposals sponsored by the most prominent corporate gadflies has dropped from 29 percent to 24 percent. In 2013, the latter figure represents just two investors, John Chevedden (and family members and his family trust) and William Steiner (and his son Kenneth). In turn, the share of proposals sponsored by other individual investors has increased from 12 percent to 19 percent in 2013; notably, one-third of these proposals were backed by less regular gadfly investors, Gerald Armstrong and James McRitchie, as well as social investor John Harrington (who also files proposals through his social-investing fund, Harrington Investments).

*To date, 94 companies filed

The percentage of shareholder proposals sponsored by labor-union pension funds has dropped from 36 percent in 2012 to 31 percent, to date, in 2013. This decline is almost entirely attributable to less activity from private-sector labor-union funds, which sponsored 14 percent of all shareholder proposals in 2012 but have only sponsored 5 percent, to date, in 2013. While the AFL-CIO and International Brotherhood of Electrical Workers have remained active this year, two other historically regular shareholder-proposal sponsors, the Teamsters and the United Brotherhood of Carpenters, have not yet filed any proposals in 2013—though, again, their absence may be merely a function of sample bias associated with the companies holding early annual meetings.

The percentage of shareholder proposals sponsored by religious, public-policy, and social investors in 2013, 25 percent, is up from 2012 (22 percent), with relatively more proposals being introduced this year by both social-investing funds and religious institutions. This increase in religious institutions’ activity—with the share of proposals introduced by such groups up from 3 percent to 5 percent—is attributable to the reemergence of Catholic orders of nuns in the shareholder-proposal process in 2013. After sponsoring between 11 and 19 proposals annually from 2006 through 2011, Catholic orders of nuns introduced only three proposals in all of 2012, but they have already sponsored five to date this year: three proposals on corporate lobbying introduced by the Missionary Oblates of Mary Immaculate and the Sisters of St. Francis, one on human rights by the Loretto Literary and Benevolence Institution, and one on genetically engineered organisms by the Sisters of Charity of St. Elizabeth.

*To date, 94 companies filed

In keeping with historical trends, institutional investors without a religious, social, or public-policy orientation or a connection to organized labor have played virtually no role in the shareholder-proposal process. The sole proposal introduced by such investors this year was introduced at the energy company Hess by the hedge fund Elliott Associates,[16] which has launched a proxy fight seeking to elect its own slate of alternative directors at the company’s May 16 meeting.[17] Elliott has acquired over $800 million in Hess’s common stock,[18] and it claims that its alternative directors could help to improve the performance of a company that, according to Elliott’s proxy materials, has underperformed peers by 332.9 percent over the 17 years that it has been led by chief executive John Hess.[19] Elliott’s proposal would “repeal any provisions or amendments of the company’s by-laws adopted without stockholder approval after February 2, 2011 and prior to the company’s 2013 annual meeting.”[20] Since Hess represents that no such amendments have been made,[21] Elliott’s proposal seems designed to block any possible defenses to Elliott’s proxy fight that the board might adopt in advance of the annual meeting.

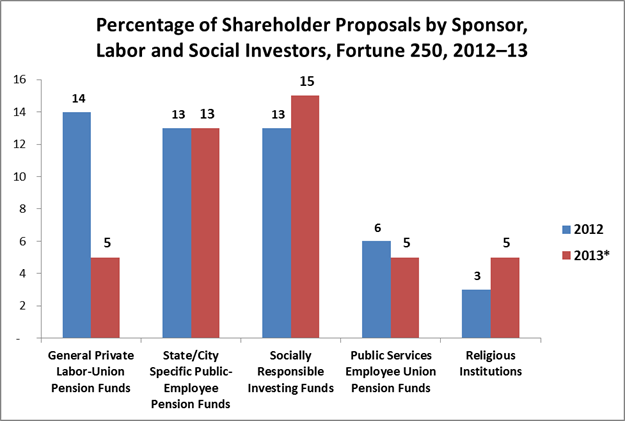

In total, seven shareholders have introduced four or more proposals to date in 2013: the corporate gadflies Chevedden and Steiner; labor funds associated with the AFL-CIO, AFSCME, and New York state employees; and the social-investing funds Northstar Asset Management and Harrington Investments (including John Harrington’s individually introduced proposals). The most common sponsors, other than Chevedden and Steiner, have been AFSCME and the New York State fund.

Shareholder-Proposal and Executive-Compensation Advisory Votes, 2013

As of April 12, 20 companies in the Proxy Monitor database have held annual meetings, considering 19 shareholder proposals in addition to shareholder advisory votes on executive compensation. Three of the 19 shareholder proposals have received majority support, each calling on companies to declassify their boards and elect all directors annually—a class of proposal that has typically earned broad shareholder support because shareholders perceive staggered boards as impediments to corporate takeover bids.[22] (These proposals were sponsored by Pension Reserves Investment Management, which oversees Massachusetts public employees’ pensions,[23] at three companies meeting on January 24: Air Products & Chemicals, Costco, and Jacobs Engineering—receiving the backing of 81 percent, 72 percent, and 82 percent of shareholders, respectively.)

Only one other shareholder proposal received at least 40 percent support from shareholders: a proposal concerning the vesting of management equity awards in the event of a change of control, which was introduced at Walgreen’s January 9 meeting by the labor-union-owned Amalgamated Bank[24] and which received 41 percent shareholder backing. At its March 6 meeting, Walt Disney faced the first 2013 shareholder proposal seeking “proxy access” (granting shareholders the right to nominate directors on corporate proxy ballots), which was introduced by Hermes Equity Ownership Services, which focuses on activist investment seeking “sustainability” for the largest British pension fund.[25] The proposal received just under 40 percent of the shareholder vote.[26] (The low sample size of shareholder proposals voted on to date makes it impossible to assess changes in shareholder support for any category of shareholder proposal.)[27]

A majority of shareholders supported executive-compensation packages at 19 of the 20 companies in the Proxy Monitor database that had held say-on-pay votes by April 12. The exception, Navistar International, met February 19 and received under 18 percent of shareholder support for its executive compensation. Navistar, which had seen its share price drop from $40.29 to $24.05 between the record dates for its 2012 and 2013 meetings, was under significant pressure from shareholder activist Carl Icahn, who holds 15 percent of the company’s stock and sent the board a letter last September calling it “asleep at the switch” and objecting to its process for hiring interim chief executive Lewis Campbell.[28] Icahn, along with Mario Gabelli of Gamco Investors (owners of over 6 percent of the company’s shares), also objected to the board’s adoption of an anti-takeover poison pill.[29] To head off a proxy fight, Navistar added three Icahn-backed directors to its board;[30] and on March 7, the company named Troy Clarke its permanent chief executive and announced earnings that beat expectations—driving up the company’s share price by 27 percent.[31]

Aside from Navistar, the company receiving the lowest shareholder support for its executive compensation was Disney, which received 58 percent at its March 6 meeting. Whereas Navistar’s decisive Against vote was driven by shareholder activists like Icahn and Gabelli holding large investment stakes—and in the wake of abysmal share-price performance, CEO turnover, and board anti-takeover actions—Disney’s atypically high share of votes Against seems to have been primarily pushed by the California State Teachers’ Retirement System (CalSTRS), the nation’s second-largest pension fund, which engaged in a back-and-forth with Disney’s management objecting to its pay practices;[32] and by the proxy-advisory firm ISS, whose Against recommendation tends to translate into a 15-percentage-point increase in Against shareholder votes.[33] Whatever the merits of CalSTRS’s and ISS’s objections to Disney’s pay package, shareholders’ ultimate majority support is perhaps unsurprising in light of the fact that the company’s share price rose from $38.40 to $50.97 between its 2012 and 2013 record dates.

The only other companies in the Proxy Monitor database to receive shareholder support under 90 percent to date in 2013 are Apple (February 27, 61 percent), Hewlett-Packard (March 20, 76 percent), and Starbucks (March 20, 72 percent). ISS recommended that shareholders vote Against executive pay at both Apple and Starbucks. ISS initially recommended a vote Against pay at Hewlett-Packard, changing its recommendation after the company made some modifications, on March 12[34]—a date presumably after votes were cast by at least some of ISS’s client shareholders.[35]

What to Watch For

As proxy season begins in earnest, shareholders at companies in the Proxy Monitor database will face votes on many more shareholder proposals in each of the four major categories of interest identified in the Winter Report: splitting the chairman and CEO, political spending and lobbying, board declassification, and proxy access.

Splitting the Chairman and CEO

While most headlines have focused on JPMorgan Chase’s proposal to split its chairman and CEO roles, up for a vote on May 21, at least 16 other Fortune 250 companies that are meeting face similar proposals between now and then (companies listed are those that had filed proxy materials with the SEC at the time this report was written):

- U.S. Bancorp, meeting April 16;

- Honeywell, meeting April 22;

- DuPont, meeting April 24;

- General Electric, meeting April 24;

- Textron, meeting April 24;

- Edison International, meeting April 25;

- Johnson & Johnson, meeting April 25;

- Lockheed Martin, meeting April 25;

- Abbott Laboratories, meeting April 26;

- AT&T, meeting April 26;

- American Express, meeting April 29;

- Boeing, meeting April 29;

- IBM, meeting April 30;

- DIRECTV, meeting May 2;

- Sempra Energy, meeting May 9; and

- Hess, meeting May 16.

Political Spending and Lobbying

Notwithstanding that 2013, unlike 2012, is not a federal-election year, the share of proposals revolving around political spending or lobbying has increased this year—though perhaps unsurprisingly, this year’s proposals are more likely to focus on lobbying and trade-association memberships than corporations’ contributions to the political process. Only five Fortune 250 companies meeting between April 15 and May 16 face proposals seeking disclosure related simply to corporate political spending:[36]

- Humana, meeting April 25;

- AT&T, meeting April 26;

- Motorola, meeting May 6;

- Anadarko Petroleum, meeting May 14; and

- Hess, meeting May 16.

Another four companies face a new class of proposals, sponsored by the social-investing fund Northstar Asset Management, asking them to prepare a report on “corporate values and political spending”:

- Praxair, meeting April 23;

- Johnson & Johnson, meeting April 25;

- Chubb, meeting April 30; and

- EMC, meeting May 1.

Significantly more companies, however—13—face proposals asking them to prepare reports disclosing various lobbying practices and priorities and, in some cases, payments—including to trade associations:

- eBay, meeting April 18;

- American Electric Power, meeting April 23;

- Cigna, meeting April 24;

- Citigroup, meeting April 24;

- DuPont, meeting April 24;

- Marathon Oil, meeting April 24;

- Lockheed Martin, meeting April 25;

- Abbott Laboratories, meeting April 26;

- IBM, meeting April 30;

- General Dynamics, meeting May 1;

- United Parcel Service, meeting May 2;

- Valero Energy, meeting May 2; and

- Verizon, meeting May 2.

Board Declassification

Because most large companies already elect all their directors annually, proposals seeking to declassify boards are less numerous than many other classes of proposals—but remain the most likely class of proposals to pass. Four companies face proposals seeking to declassify their boards, instead electing directors annually:

- Kellogg, meeting April 26;

- PACCAR, meeting April 29;

- U.S. Steel, meeting April 30; and

- Huntsman Corporation, meeting May 2.

Proxy Access

Although these proposals remain rare, the fact that they would potentially create contested director elections—and that the SEC previously adopted a proxy-access rule, subsequently vacated by the U.S. Court of Appeals for the D.C. Circuit[37]—makes them salient. Verizon faces a proxy-access proposal at its May 2 meeting, tracking the rule previously adopted by the SEC.

This report analyzes information gathered from the Manhattan Institute’s ProxyMonitor.org database, which contains information relating to all shareholder proposals submitted for shareholder vote since 2006, for the 250 largest American public companies by revenues.

ENDNOTES

- Pub. L. No. 111-203, 124 Stat. 1376, §951 (2010) [hereinafter Dodd-Frank Act].

- See Proxy Monitor, Reports and Findings, http://proxymonitor.org/Forms/reports_findings.aspx (last visited Apr. 11, 2013).

- Wikipedia, Tax Day, http://en.wikipedia.org/wiki/Tax_Day (last visited Apr. 11, 2013).

- James R. Copland, Political Spending, Say on Pay, and Other Key Issues to Watch in the 2013 Proxy Season (Manhattan Inst. for Pol’y Res., Winter 2013), http://proxymonitor.org/Forms/pmr_05.aspx (highlighting these proposals as ones to watch in 2013).

- Dodd-Frank Act, supra note 1.

- While the percentage of shareholder proposals related to corporate lobbying and political spending has increased only slightly in 2013, relative to 2012, the nature of such proposals is different this year. In 2012, two-thirds of such proposals related to corporate political spending, with most seeking additional disclosures of such spending along the lines advocated by Bruce Freed’s Center for Political Accountability. In 2013, a majority of proposals in this category have related to corporate lobbying, and only 21 percent have sought that companies report or disclose political spending. This shift is probably attributable to the fact that 2013, unlike 2012, is not a federal-election year.

a. Also, in 2013, the social-investing fund Northstar Asset Management’s proposals in this area have asked companies to provide a “report on corporate values and political contributions.” In 2012, its proposals sought shareholder advisory votes on corporate political spending, but these proposals received minimal shareholder support.

- Subsequent to the empirical analysis conducted for this report, the Humane Society introduced an animal-rights-related proposal related to the sale of products containing fur at Kohl’s, scheduled to meet May 16.

- See Lucian A. Bebchuk, Alma Cohen & Charles C.Y. Wang, Staggered Boards and the Wealth of Shareholders: Evidence from Two Natural Experiments (Nat'l Bureau of Econ. Research, Working Paper No. 17127, June 2011), available at http://www.nber.org/papers/w17127.

- Joseph A. Giannone, Investor Gadfly Davis Calls It Quits ... for Now, Reuters (Apr. 19, 2012), http://www.reuters.com/article/2012/04/19/us-corporategovernance-davis-idUSBRE83I1CS20120419.

- See Copland, Proxy Monitor 2012: A Report on Corporate Governance and Shareholder Activism, 14 (Manhattan Inst. for Pol’y Res., Fall 2012); Ross Kerber, AFSCME Eyes Dual Chairman-CEO Roles at JPMorgan, Goldman, Huffington Post (Jan. 17, 2012), http://www.huffingtonpost.com/2012/01/17/afscme-chairman-ceo-roles_n_1209924.html.

- See, e.g., Business Roundtable & Chamber of Commerce of the U.S. v. SEC, 647 F.3d 1144, 1152 (D.C. Cir. 2011), http://www.cadc.uscourts.gov/internet/opinions.nsf/89BE4D084BA5EBDA852578D5004FBBBE/$file/10-1305-1320103.pdf (citing proposition that “unions and state and local governments whose interests in jobs may well be greater than their interest in share value, can be expected to pursue self-interested objectives rather than the goal of maximizing shareholder value”); see also OIG Department of Labor Report, Proxy-Voting May Not Be Solely for the Economic Benefit of Retirement Plans, Rpt. No. 09-11-001-12-121, intro “Briefly” (Mar. 31, 2011), http://www.oig.dol.gov/public/reports/oa/2011/09-11-001-12-121.pdf (questioning whether labor pension funds are using “plan assets to support or pursue proxy proposals for personal, social, legislative, regulatory, or public policy agendas”).

- Anthony Derosa, Exclusive: Goldman Sachs reaches deal to halt move to split top roles, Reuters (Apr. 10, 2013), http://live.reuters.com/Event/Business/72021200.

- Susanne Craig & Jessica Silver-Greenberg, JPMorgan Works to Avert Split of Chief and Chairman Roles, N.Y. Times Dealbook (Apr. 5, 2013), http://dealbook.nytimes.com/2013/04/05/behind-the-scenes-jpmorgan-works-to-sway-shareholders-on-dimon-vote/?ref=jamesdimon.

- See, e.g., James A. Brickley, Jeffrey L. Coles & Gregg Jarrell, Leadership Structure: Separating the CEO and Chairman of the Board, 3 J. Corp. Fin. 189 (1997) (finding no evidence that separating chairman and CEO roles improves financial performance); B. Ram Baliga, R. Charles Moyer & Ramesh S. Rao, CEO Duality and Firm Performance: What’s the Fuss?, 17 Strategic Mgmt. J. 41 (1996) (finding no evidence of stock improvements after companies separated chairman and CEO positions); Lex Donaldson & James H. Davis, Stewardship Theory or Agency Theory: CEO Governance and Shareholder Returns, 16 Austl. J. Mgmt. 49 (1991) (finding evidence of higher stock returns for companies with dual chairmen-CEOs than those with separate positions). But see Steven Balsam, John Puthenpurackal & Arun Upadhyay, The Determinants and Performance Impact of Outside Board Leadership, working paper, Dec. 22, 2011, http://papers.ssrn.com/sol3/papers.cfm?abstract_id=1361255; Brian K. Boyd, CEO Duality and Firm Performance: A Contingency Model, 16 Strategic Mgmt. J. 301 (1995) (finding slight improvements in the financial performance of the entire set of companies studied but significant industry-to-industry variance).

- See Copland, supra note 10, at 23; see also Craig and Silver-Greenberg, supra note 13 (observing that Oppenheimer Funds tends to vote its shares consistent with ISS’s recommendation).

- Elliott founder and principal Paul Singer is the chairman of the Manhattan Institute for Policy Research. Neither Mr. Singer nor any employee or agent of Elliott has discussed Hess or the fund’s proxy fight with the author of this report.

- Hess Corporation, Preliminary Proxy Statement Pursuant to Section 14(a) of the Securities Exchange Act of 1934, proposal 8 at 33 (2013), available at http://www.sec.gov/Archives/edgar/data/4447/000104746913003661/a2214159zprrn14a.htm.

- See id. at 23.

- See id. at 31.

- Hess Corporation, Proxy Statement Pursuant to Section 14(a) of the Securities Exchange Act of 1934, proposal 8 at 86 (March 21, 2013), available at http://www.sec.gov/Archives/edgar/data/4447/000119312513119720/d475998ddefc14a.htm.

- See id.

- Cf. Lucian A. Bebchuk & Alma Cohen, The Costs of Entrenched Boards, 78 J. Fin. Econ. 409, 410 (2005) (finding that “controlling for firm characteristics including other governance provisions, staggered boards are associated with a reduced firm value”).

- See Pension Reserves Investment Management Board, http://www.mapension.com (last visited Apr. 12, 2013).

- See Amalgamated Bank, About Us, http://www.amalgamatedbank.com/home/aboutus (last visited Apr. 11, 2013).

- See Eurosif, Hermes Equity Ownership Services Ltd., http://www.eurosif.org/network/list-of-member-affiliates/item/292-hermes (last visited Apr. 11, 2013).

- While Disney is the only Fortune 250 company yet to vote on a shareholder-sponsored proxy-access proposal, Hewlett-Packard’s management introduced its own proxy-access proposal at its March 20 meeting, which received overwhelming shareholder support.

- The three chairman-independence proposals introduced to date have received, on average, 25 percent support—down from an average of 34 percent in 2012—but the small number of votes makes it difficult to point to a trend, particularly since the 2013 number is skewed by the proposal at Whole Foods, which currently separates the chairman and CEO roles and where the proposal only received 10 percent of the vote. Only two political-spending or lobbying proposals have been voted on to date, a proposal requesting that Visa prepare a report on its lobbying and trade-association expenses, which received 31 percent support; and a proposal seeking to prohibit political spending by Starbucks, which received 4 percent support.

- See David Eaton, Navistar Off Course, According to Icahn, Glass Lewis & Co. (Sept. 11, 2012), http://www.glasslewis.com/blog/navistar-off-course-according-to-icahn/.

- See Paul Merrion, Gabelli urges Navistar to drop poison pill, Crain’s Chi. Bus. (Oct. 25, 2012), http://www.chicagobusiness.com/article/20121025/NEWS05/121029873/gabelli-urges-navistar-to-drop-poison-pill.

- See Industry News, Navistar names Icahn managing director to board, Crain’s Chi. Bus. (Dec. 12, 2012), http://www.chicagobusiness.com/article/20121212/NEWS05/121219923/navistar-names-icahn-managing-director-to-board.

- See Alejandra Cancino, Navistar names new CEO; stock up 27% on earnings: Lewis Campbell stepping down as interim CEO and from board, Chi. Trib. (Mar. 7, 2013) available at http://articles.chicagotribune.com/2013-03-07/business/chi-navistar-names-new-ceo-as-it-reports-loss-20130307_1_dan-ustian-navistar-plans-13-liter-engines.

- See The Walt Disney Company, Notice of Exempt Solicitation: Letter from CalSTRS and PGGM Investments, SEC (Feb. 26, 2013) available at http://www.sec.gov/Archives/edgar/data/1001039/000095015913000137/disneypx14a6g.htm; The Walt Disney Company, Proxy Statement Pursuant to Section 14(a) of the Securities Exchange Act of 1934 (March 21, 2013), available at http://www.sec.gov/Archives/edgar/data/1001039/000120677413000786/waltdisney_defa14a.htm; The Walt Disney Company, Notice of Exempt Solicitation: Disney Shareholder Letter, SEC (2013) available at http://www.sec.gov/Archives/edgar/data/1001039/000095015913000139/disneypx14a6g.htm.

- See Copland, supra note 10, at 20-21.

- See Hewlett-Packard Company, Proxy Statement Pursuant to Section 14(a) of the Securities Exchange Act of 1934, News Release: HP Issues Statement on ISS Recommendation, SEC (Mar. 12, 2013), available at http://www.sec.gov/Archives/edgar/data/47217/000110465913019801/a13-7340_1defa14a.htm.

- Cf. Barry B. Burr, Florida board, AFSCME pension plan reveal Hewlett-Packard votes, Pensions & Investments (Mar. 11, 2013), http://www.pionline.com/article/20130311/DAILYREG/130319993/florida-board-afscme-pension-plan-reveal-hewlett-packard-votes&template=print (announcing that the Florida State Board of Administration and the AFSCME pension plans were voting against Hewlett-Packard’s executive-compensation packages).

- These proposals follow the general format advocated by Bruce Freed’s Center for Political Accountability; see Center for Political Accountability, http://www.politicalaccountability.net (last visited Apr. 11, 2013).

- See Business Roundtable v. SEC, supra note 11 (rejecting as arbitrary and capricious the SEC’s adoption of a proxy-access rule); see also Facilitating Shareholder Director Nominations, SEC Rel. No. 34-62764 (Aug. 25, 2010), http://www.sec.gov/rules/final/2010/33-9136.pdf.